Introduction

Saudi Prince al-Waleed bin Talal al-Saud has a net worth of $20 billion. Such wealth places him first on the Forbes’ 2011 list of World's Billionaires for the Middle East region. Who manages the Prince’s money? The Prince does. The rich tend to rely on the “balanced portfolio, 401(k) and insurance” wealth management firms less and less. The Middle East’s wealthy number less in headcounts and hold more in assets. Such a concentration of wealth has made them a very attractive target for wealth management firms. The Middle Eastern affluent, rich and super-rich also tend to hold their money abroad, invest most in hard assets (like real estate and commodities) and make large- scale personal investments in foreign companies — making them a very coveted target for the likes of UBS and Merrill Lynch. Yet, the present cherry-picking model of customer acquisition will reach its limits — as the wealth spreads out and Middle Eastern banks learn how to offer Western-style wealth management services.

Middle Eastern policymakers and bankers will develop an indigenous wealth management industry which keeps the super-wealthy’s investments at home. Developing a local national wealth management industry requires letting in foreign competition, changing banking and securities laws, and growing local companies whose shares are worth buying. The first part of the article reviews trends in wealth and wealth management in the Middle East and North African (MENA) region. We show that $800 billion lies-in-waiting for ambitious wealth managers to prospect. We show that foreign wealth managers will continue to capture the lion’s share of this wealth because most local banks can not compete. In the article’s second part, we show why Turkey has succeeded in growing a nationally and internationally competitive wealth management industry — whereas Saudi Arabia’s remains less than perfect. The Turkish policy and the Turkish wealth management industry have succeeded to some extent, because they have grown the pool of the wealth. Whereas the Saudi super-rich contently send their money abroad, their Turkish counterparts use their funds to develop local industry, though they also send quite a lot abroad. In the third section, we describe how policymakers can help bring the billions abroad home by making business easier, reforming banking and securities law, and forcing local banks to become more efficient. In the last section, we describe how foreign wealth management firms can increase their assets under management in the region. These multi-trillion dollar mammoths should use their negotiating power to open MENA markets and grow local multi-millionaires.

The Wealth Management Industry in Perspective

The wealth management industry in the Middle East and North Africa (MENA) represents a roughly $800 billion opportunity. Figure 1 shows the total amount of assets in the hands of affluent individuals (with more than $100,000 in investable assets), high net worth individuals (dollar millionaires or HNWIs as those in the financial industry call them), and ultra-high net worth individuals (the UHNWIs, which have at least $30 million in investable assets). As the figure shows, wealth in the region lies mostly in Turkey and Saudi Arabia — two countries that we discuss in-depth in the next section. Egypt and the United Arab Emirates (UAE) represent a second tier for wealth management firms — with roughly $60 billion to $110 billion in investable assets in the hands of the richest 10% of the population in each country. The other countries in the region represent ancillary markets, with roughly $20 billion in assets each — or the amount of wealth required to make the top 50 in the Forbes 1000.

In the Middle East, most assets lie in the hands of very few ultra-high net worth individuals. According to the annual Merrill Lynch-Cap Gemini World Wealth Report for various years, North American and European wealth tends to spread out at roughly a ratio of $3 million to every ultra and regular high net worth individual in the region. The MENA region — despite the World Wealth’s Report’s data — has ratios closer to 7-to-1. The high concentration of wealth in the region provides wealth management and private banking firms a unique opportunity to service relatively few ultra-high net worth clients without the expense of servicing large numbers of clients. Moreover, the political uprisings in the region will likely do little to dampen accumulation of wealth in the region. Several studies — the Steiner (2010) study being the most prominent — show (rather counter-intuitively) that political uprising has little effect on foreign investment.

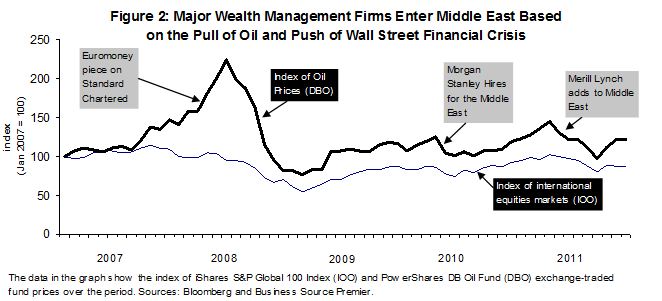

The rise of the wealth management industry in the MENA region has been caused by the better than average returns to oil investments (combined with their relative volatility). Figure 2 shows the way that overall equity prices and oil prices have changed in roughly the last 5 years. During the period, oil prices almost doubled at their peak in 2008 and halved again in about the same year. In contrast, global equity prices in general did not fall as much. The standard deviation (the measure of volatility in these prices and thus a proxy for risk) was 1.6 times higher for oil than for equities. Higher standard deviations for oil prices, and thus incomes based on oil, imply that the Middle East’s wealthy require wealth managers who can help them ride out these waves of uncertainty.

These dramatic changes in the sources of Middle Eastern wealth — and relatively lack-lustre returns on equities in global equity markets — probably drove the Western broker-dealer to enter Middle Eastern markets more aggressively, rather than to wait for the Middle East’s ultra-wealthy to come to them in Europe. On the figure, we show some of the many announcements by foreign broker-dealers who increased staff or investments in wealth management offerings in the Middle East or both. As of 2012, most of their major global banks offer wealth management and private banking in the Middle East.

Global investment houses have expanded their offerings in the Middle East. Such entry — particularly by foreign wealth management firms — exacerbates an already existing tendency for investors in the MENA region to invest abroad. Middle Easterners send roughly 70% of their wealth overseas, as opposed to the US and Japan’s 3% and Western Europe’s 25% (Maude, 2006). More recent estimates by the Boston Consulting Group place the off-shoring of wealth management-related assets at about 50% (Becerra, 2011).

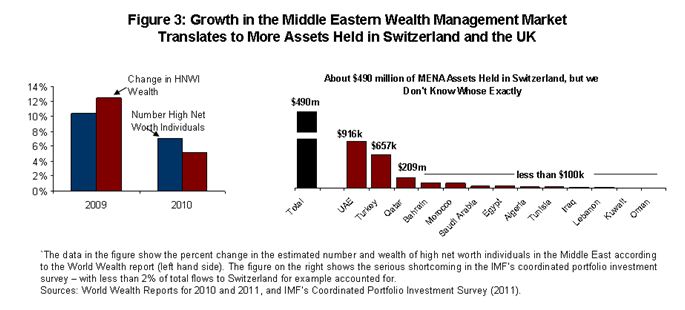

Yet, academics and policymakers know very little about whose wealth specifically goes where. Figure 3 shows that estimates for the Middle East region indicate that both the number of wealthy individuals grew — and the amount of wealth grew about 10% in 2009 and about 5% in 2010. Of that increase, most wealth management watchers (like the Boston Consulting Group and Merrill Lynch-Cap Gemini) place most of that money in Switzerland and the UK. Yet, IMF data fail to show exactly who invests these funds and from where. According to available data, Emirati, Turkish, and Qatari investors place the largest amount of their portfolios in Switzerland. Yet, the IMF data, showing $1.5 million in placements, fall far short of the estimated $500,000 in Swiss accounts. Such data suggest that the IMF needs to collect better data (rather than anything specific about wealth management clients from the region).

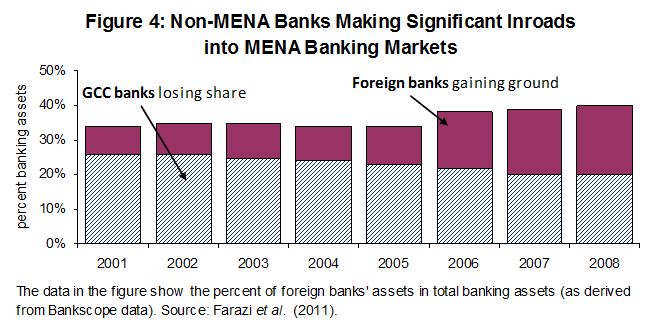

The limited data available suggest that these wealth management firms are increasingly trying to operate directly in MENA countries. Figure 4 shows that foreign banks have increasingly been participating in Middle Eastern markets. At the beginning of the decade, foreign banks comprised only about 10% of the total market by assets. Banks coming from the Arabian Peninsula from the member countries of the Gulf Cooperation Council comprised about 27% of assets. By the end of the decade, foreign banks made significant progress — taking about 20% of the market. Such a trend suggests that Western banks are seeking to capture a larger share of the Middle Easterners’ wallet — moving from wealth management to a broader range of banking services. We do not know that all these banks offer wealth management. But, as wealth management comprises the most attractive banking sector, we can deduce that a fair share of this increase owes to foreign interest in finding wealth management and private banking customers.

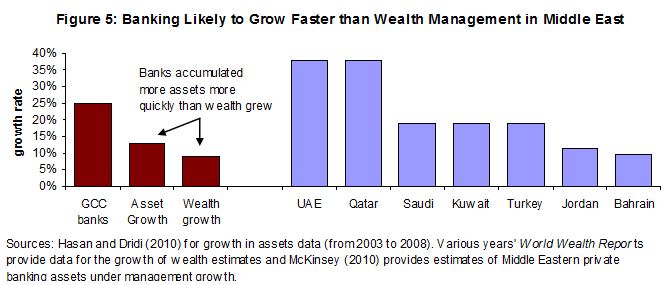

If foreign wealth management firms (particularly in the UK and Switzerland) have managed to capture the local market, then local wealth management services remain extremely under-developed. VRL (2010), a private consulting company, has indentified the 32 banks in the region in their profile of wealth management services in the region. Yet, looking at their balance sheets, much of their growth still comes from plain vanilla banking. Figure 5 shows that the less glamorous business-as-usual banking led to faster growth of assets under management (the goal of every banker) than wealth growth in the region (and faster than wealth managers could attract that wealth) for 2003–2008. As shown, Arabian Peninsula banks grew their assets by about 25% over the second half of the 2000s. Assets under management by private bankers and wealth managers increased by about 12%, according to Merrill Lynch-Cap Gemini estimates. Wealth grew in the region as a whole by about 10%.

Could these trends suggest that investments in plain old banking in the region could yield higher growth rates and larger volumes of assets under management than playing in an increasingly crowded wealth management sector? In the UAE and Qatar (two already highly developed financial markets), banking assets grew by about 35% (as more of the middle class became affluent). These patterns, judging by past data, seem unlikely to change in the near future. Our two comparator countries for the next section — Turkey and Saudi Arabia — saw banking assets grow (as a percent of GDP) by almost double the estimated growth rate of wealth in the region. Both these growth rates far exceed the growth rates which appear in the wealth management industry estimates.

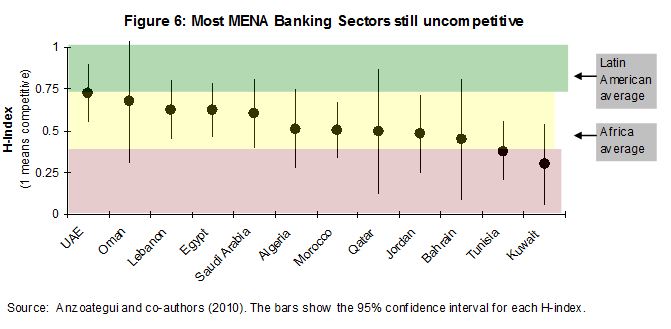

Non-competitive banking sectors across the region provide one explanation why local banks remain under-developed…and why foreign banks hold off from making large-scale investments in Middle Eastern wealth management service offerings. Anzoategui and co-authors (2010), in a study of the MENA banking, describe prevailing market conditions as “monopolistic competition.” Figure 6 shows a popular measure of competitiveness — known as the H-Index. An H-Index looks at the extent to which banks pass along increasing costs by raising fees. Only banks that do not compete at bare-bones profit margins of a highly competitive market have the luxury of absorbing parts of these cost increases. An H-Index measures the extent to which a bank absorbs these cost increases rather than passes them along. The Anzoategui et al. data show that only UAE (and maybe Omani) banks likely operate in a highly competitive environment. Kuwaiti and Turkish banks seem the most insulated. Other authors corroborate these findings. Abbasoglu et al. (2007) find that Turkish banks became increasingly monopolistic in the 2000s — with falling H-index values from roughly 0.6 to 0.3.

Another reason for the under-development of local banking (and thus an indigenous wealth management industry) may be due to the lack of profitable investment opportunities in the region. Banks must take savings — including the savings of ultra-high net worth individuals — and place these funds into profitable investments. Yet, according to regression analysis by Hasan and Dridi (2010), bank profitability in the MENA region has decreased as bank investment portfolios grow. Looking at time series data for the MENA region from 2007 to 2009, they find a statistically significant negative correlation between banks’ investment portfolio sizes (as a percent of total assets) and bank profitability. They also find a positive relationship between bank profitability and the percent of real estate and construction lending in banks’ portfolios (which hind-sight tells us resulted from the economics of bubble financing). These results — when taken together — suggest that MENA banks in countries discussed by the authors tend to destroy value when they invest in MENA markets.

These results may explain why most MENA-based investment funds and the wealth managers that use these funds do not invest in the MENA region. In a recent study, Mako and Sourrouille (2010) analysed the level of inter-MENA region portfolio investment. Investment companies, in 5 out of the 11 countries they looked at, have significant investments in the MENA region. Of these, Bahraini investors hold the most, with $276 million or 23% of their portfolios. Saudi Arabia — the largest economy in the region (outside of Turkey) — invested only $71 million in the MENA region in 2009 (or less than 1%). On a similar scale (through a much larger proportion), the UAE funds invested $92 million in the MENA region, representing roughly 12% of invested funds.

The contrast between the MENA region’s two largest countries (excluding Israel) provides some insight into the opportunities and potential pitfalls of expanding wealth management services in the Middle East. Turkey represents an example of a successful locally grown wealth management industry. Saudi Arabia represents an under-developed wealth management industry — one which foreign banks still spirit away funds rather than invest them locally. Such wealth management practices have led to a lack of funding to expand Saudi markets for locally-produced affluent, high and ultra-high net worth individuals.

Comparing the Region's Two Key Private Wealth Prospects: Turkey and Saudi Arabia

Comparing Turkish and Saudi wealth creation provides a fascinating glimpse at (and forecast of) the future of wealth management in both countries. Both economies have organised family interests which control large shares of the economy. However, in Turkey, these family-oriented interests focus on local productive economic activities which generate wealth. In Saudi Arabia, these family interests tend to invest resource gains abroad.

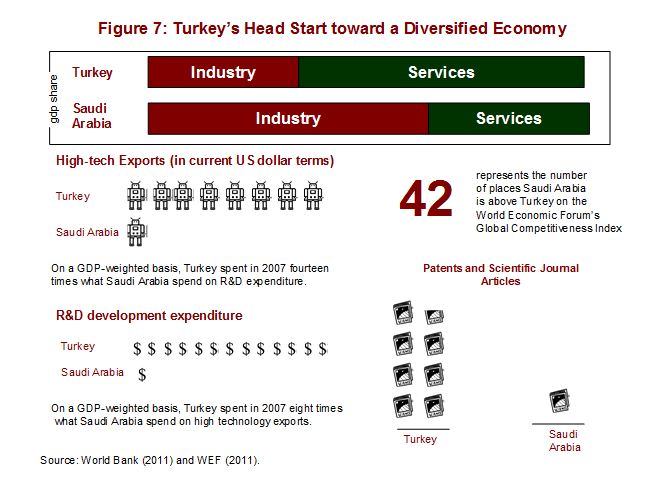

Saudi Arabian companies (and the ultra-high net worth individuals that own and control them) tend to invest less in diversified and high-tech sectors, which will create a larger class of affluent bank clients. Figure 7 provides an extremely unrigorous (though illustrative) overview of the differences in investment behaviour between Saudi Arabia and Turkey. The majority of Turkish economic activity (as measured in percent of GDP) focused on services rather than industry in 2010. In Saudi Arabia, most productive enterprise (the result of previous investment decisions) still centres around industry, particularly the oil sector. Saudi Arabian business — at least according to the World Economic Forum — ranks 42 places above Turkish business. However, such competitiveness will likely increase the wealth of Saudi Arabia’s existing wealthy — rather than create more dollar millionaires. Looking at the high-tech and R&D-based industries, which have made many of the US’s and Europe’s millionaires, provides a clue about the way future economic growth will translate into future private wealth clients. In 2007 (the latest year data are available), Turkish high-tech exports outstripped Saudi ones by a ratio of roughly 8-to-1. Turkish companies’ R&D expenditure — investment needed to promote sustainable growth and economic diversification — eclipsed Saudi expenditure by about 13-to-1. Turkish patents and scientific journal articles outnumbered Saudi ones by about 7.5-to-1. Keeping in mind the usual caveats about arguing using selected cases, Turkish companies seem to make the types of investments which much of the literature suggest lead to higher and more wide-spread incomes.

Such differences in the sources of wealth in the two countries have created rather different distributions of wealth in both countries among ultra-high net worth individuals (the richest according to the popular press stories we reviewed). As shown in Figure 8, Turkey’s richest are about one-eighth as rich as their Saudi counterparts despite having an economy roughly 1.6 times as large. Naturally, drawing conclusions from popular press accounts of the rich-and-famous provides little scientifically credible evidence. However, from a practical perspective, the wealth manager who wins the Bin Laden family’s account will have almost 8 times more assets under management (and the associated fees) than the one who lands the Zorlu account.

A look at Turkey’s and Saudi’s richest families reveals other trends of interest to wealth managers looking to land accounts like these. Unlike in Turkey, many of Saudi Arabia’s largest companies are not public. The lack of public disclosure poses a particular peril — given improved know-your-customer requirements in the major financial institutions. Turkish wealth comes from diversified companies, whereas (except for Saudi Basic Industries) most of the companies that make Saudis extremely rich focus on narrow economic sectors. Both the Kingdom Holding Company and MBI International Group and Partners make a strong point to highlight their London connections on their website.

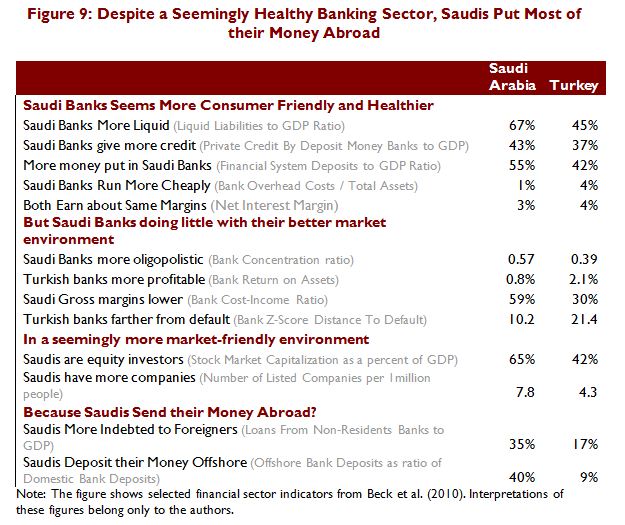

What does high-tech production and family wealth have to do with wealth management? Wealth accumulates from productive activity, and financial institutions store and channel the proceeds of constructive activity. A healthy local banking sector promotes internal investment, and thus, the creation of more HNWIs. A healthy local banking sector can also compete effectively against foreign wealth management companies. As shown in Figure 9, the Saudi banking sector looks just as healthy — if not healthier — than the Turkish banking sector in 2010. Saudi banks had more liquid liabilities and more deposits to cover them. Saudi banks operated in a more oligopolistic market with higher market capitalisation ratios (as a percent of GDP) than their Turkish cousins.

Saudis save more than Turks do — and they save it offshore. As a share of GDP, both Turkish and Saudi private investment equalled about 20% of GDP in 2010. Yet, Saudis saved 43% of their GDP — whereas Turks saved only 14% in 2010. Such savings translate into wealth management accounts which find their way to Switzerland and the UK. Savings — if we resort to high macroeconomic theory — signal a lack of productive investment, consumption options, or a desire to put money aside for a rainy day. Saudi authorities clearly want to save for a time when their oil-reserves run out, as evidenced by their roughly $500 billion sovereign wealth fund. The Turks want to grow their economy today.

Saudis save more than Turks do — and they save it offshore. As a share of GDP, both Turkish and Saudi private investment equalled about 20% of GDP in 2010. Yet, Saudis saved 43% of their GDP — whereas Turks saved only 14% in 2010. Such savings translate into wealth management accounts which find their way to Switzerland and the UK. Savings — if we resort to high macroeconomic theory — signal a lack of productive investment, consumption options, or a desire to put money aside for a rainy day. Saudi authorities clearly want to save for a time when their oil-reserves run out, as evidenced by their roughly $500 billion sovereign wealth fund. The Turks want to grow their economy today.

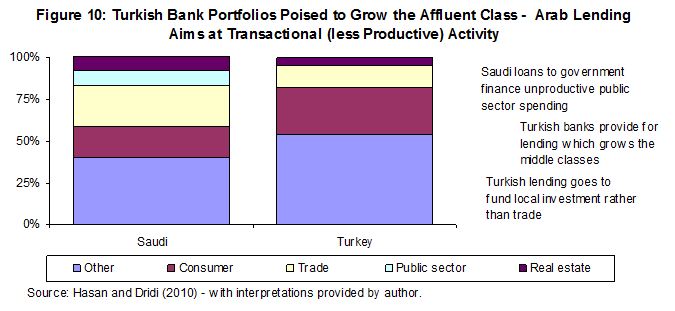

The result is that Turkish banks have already broken into the private wealth management market, whereas their Saudi colleagues still lack internal markets to develop their business. According to the Financial Times Awards for 2011, the best private banks in Turkey were both private banks Garanti and Yapi Kredi. As for best bank in the Middle East, the best were Western banks — HSBC, Standard Chartered, and Citi. Lending patterns among banks also reflect local investment priorities. As shown in Figure 10, Saudi banks allocate a much larger share of their loanable funds on trade and public sector (areas which high economic theory would describe as transactional and not directly leading to growth in economic output).

Banks should earn profits from making loans which promote private sector productivity and lead to growth. Yet, the data suggest that Saudi bank profits stem from priviledged relations with government as much as other factors. Eljelly (2009) finds that having connections to government — in the form of state ownership — positively correlates with bank performance. In contrast, Hasan and Dridi (2010) finds that government ownership of Turkish banks has no impact on bank performance.

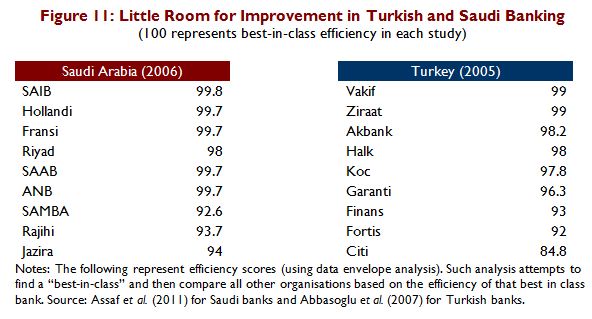

Nothing in the data suggests that differences in wealth management prospects between the two countries reflect banking efficiency. In other words, foreign wealth management firms should not expect to enter either market in order to exploit weaknesses of pre-existing rivals. Figure 11 shows the results of two separate data envelope analyses of the banking sector in each country that were conducted at about the same time. As shown, the top banks in both countries operate at very near best-in-class efficiency. The limited evidence available suggests that foreign banks did not improve Turkish bank performance (which already had very high levels of efficiency). In a study by Yildirim (2010), he finds that foreign bank acquisitions in Turkey did not lead to better bank performance.

The development of wealth management services looks far more promising in Turkey than in Saudi Arabia for three reasons. First, more Turks are likely to enter the affluent class each year than Saudis, giving aspiring wealth managers an increasing pool of prospects. Second, foreign entrants can not exploit the inefficiency (or incompetence) of local competitors in these markets like they might in places elsewhere in the Middle East. Third, differences in the prospects of wealth management in each country reflect fundamental differences in social preferences — between how much money each country saves, in which country they save these funds, and how they spend their savings when they decide to invest them.

Policy Advice for MENA Policymakers

How can the Qatars, Libyas and Lebanons of the region (those countries with fewer affluent savers) grow their own affluent, and thus, wealth management industries? The data show that they should encourage local investors to increase their investment time-horizons, particularly to invest locally rather than abroad. In their book Varieties of Capitalism, Peter Hall and David Soskice (2001) argue that economic systems’ labour, product, capital, and regulatory environments must “fit together.” The Middle East generally has labour, product market, and other policies that encourage long-term planning and investing. However, as shown in the left panel of Figure 12, most denizens of their banking sectors focus decidedly on short-term results. The average Qatari, Kuwaiti, or Saudi will want large rates of return in less than 2 years. Their Western counterparts will be content to take a longer-term view — holding investments yielding half the amount desired by the Saudi for almost 3 times as long. Such preferences yield a more “patient capitalism” which has led to long-run growth. Turkish investors tend to have higher expectations for their investments, which is understandable given recent Turkish equity price growth. However, they are also willing to wait twice as long to get these returns.[1] A client who wants to change his or her portfolio every year or two represents one of professional wealth managers’ worst nightmares.

The other key to developing the local wealth management industry, and thus, economic development, consists of encouraging ultra-high net worth individuals to bring their money home. As shown on the right-side panel of Figure 8, Middle Eastern countries which have easier business index scores (as measured by the World Bank’s Doing Business database) tend to have more patient investors. The Bahraini investor will have a longer time horizon, because doing business is easier. The Kuwaiti will have very short time horizons, partially because leaving his or her money tied up too long exposes him or her to all kinds of regulatory and business risks. Saudi Arabia proves the exception — they have short time horizons and business regulations which making doing business very easy. Making business easier should also lengthen time horizon, because Saudi, Omani, and Qatari investors know that their investments will not stagnate in a bureaucratic mire.

Changes in investment law clearly affect the ease of business and the development of a local wealth management industry. Figure 13 provides an assessment of the development of a local (national) wealth management industry — looking only at black letter banking and securities law. Not exactly surprising results emerge. Prospects look best in countries — like Jordan, Saudi Arabia and Turkey — which already have relatively well-developed financial sectors. The analysis suggests that countries like Tunisia and the UAE could develop more quickly if they generalised their zona franca approach to finance. Both countries have a financial centre with relatively few restrictions (Tangiers and Dubai respectively). Their zona franca status has allowed both countries to become wealthy quickly. However, to continue growing their wealth, and thus, their wealth management industries, they will need to extend reforms beyond isolated geographical areas. Countries like Yemen, Oman, Algeria, and Syria require nothing less than a full-scale rewriting of their banking and securities laws.

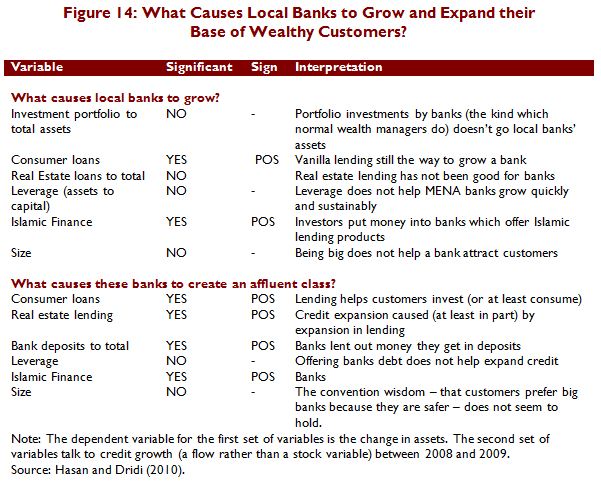

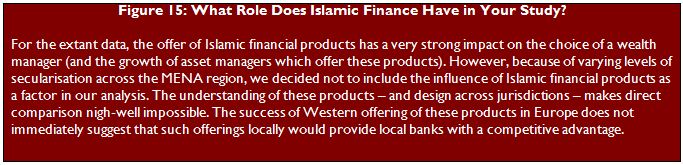

However, once the money — the savings in the hands of foreign wealth managers — comes home, these funds should be put to work in the MENA economies. Despite its lack of sex appeal, consumer lending still represents the best way of growing MENA region banks and the number of affluent savers in the region. Figure 14 shows the results of Hasan and Dridi’s (2010) regression analysis — looking at the effect of several variables on bank performance. As previous discussed, putting this money into managed accounts of stocks and bonds does little to help these banks (or economies) grow. Instead, the data show that plain vanilla lending probably still serves as the best market segment for local banks to prepare themselves for direct competition with their much larger and more sophisticated rivals in the US and Switzerland. Almost all the literature suggests that banks can increase assets under management by offering Islamic financial products. However, as we discuss in Figure 15, we do not discuss the role of such finance in this policy brief.

Significant evidence suggests that foreign participation in MENA banks can improve services, including wealth management services. Kobeissi (2010) finds a statistically significant positive relationship between the number of majority-owned foreign banks in a country and the return on bank assets, bank equity, and profitability. Abbasoglu et al. (2007) find the same phenomenon for Turkish banks — a statistically significant relationship between the presence of foreign banks and return on assets. In their regression analysis, they find that foreign ownership affected return on equity and return on assets far more than even increases in operating efficiency. Haddad and Hakim (2010) find that foreign banks did not help “import” the financial crisis into Saudi Arabia. Any attempt to protect the local financial service market likely backfired, stifling innovation.

Strategies for Foreign Wealth Management Firms

In the short-term, foreign broker-dealers entering Middle Eastern wealth management markets should focus on three things. First, they should try to capture assets held abroad rather than enter Middle Eastern markets directly. With 50–70% of wealth located in Zurich and Jersey, a wealth manager would do better to prospect for Middle Eastern money in Europe than in their clients’ home countries. Second, wealth managers should focus on the “big fish” — maximising assets under management rather than the number of clients. In this respect, the family office model will probably develop more than the financial advisor model, with roughly 50 to 500 clients per advisor in the US, Asia, and Europe. Third, they should focus on “second tier” markets — because Turkey and Saudi Arabia (while big) also have very competent competitors.

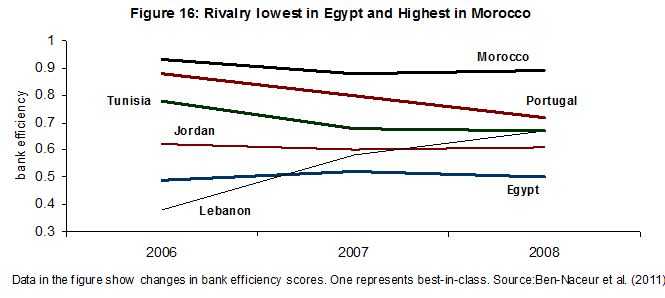

Competition is not only about market size — but also about rivalry. Figure 16 shows technical efficiency estimates for banks in the MENA region — as reported by Ben-Naceur et al. (2011). As of 2008 (for which more recent data are available), Moroccan banks pose the most serious threat to foreign entrants (having a technical efficiency above those in the authors’ comparator country Portugal). Egypt and Jordan — in terms of efficiency — seem the best targets for foreign banks (considering low efficiency of local banks and ignoring important issues like poor legislation and capital controls). These data also show that considerations about rivalry are not set in stone; technical efficiency can change significantly over time. In the time period of Ben-Naceur and his co-authors’ study, Lebanese banks made significant efficiency improvements, whereas Tunisian banks became significantly less efficient over the same time period.

The big wealth management advisors, like UBS, Barclays, and RBS, will do well to consider long-term investments in wealth-management in the Middle East. No country (with the exception of Turkey and maybe Saudi Arabia) has local banks that rival the service offerings of the big players. Barclays can offer access to derivatives, commodities (called “alternative investments in the industry”), and a range of IPOs which other firms have late access to. These companies’ analysts have access to the Boards of the companies they invest in — in a way that Middle Eastern banks cannot compete with. These firms can compete. Local financial institutions — whose management read the same Euromoney and Banker literature as the management of the global players — will want to participate in the wealth management boom. Developing these markets now will help forestall potential local competition later.

In the longer-term, the large international wealth management firms like BNP Paribas and Merrill Lynch (just to cite some examples) should develop the future HNWI segment, which comprise today’s affluent middle class. This segment will provide most of their margins in the long-term. Such development consists of engaging with local governments — encouraging them to implement the advice we give above. They do not need to engage in a social movement. As shown in Appendix II, each of the countries has an investment promotion law. Foreign asset management companies — with assets under management larger than the GDPs of most of the countries in the region — should not shy away from negotiating better and pro-economic growth access. In this way, their portfolio managers can spend a bit more time and energy finding local investments rather than jetting in from Zurich and New York.

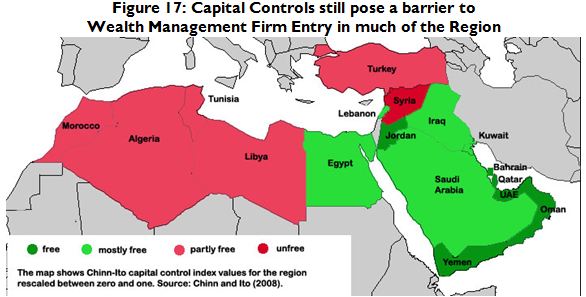

Reducing capital controls will be one of the first points of discussion between governments and these global asset management firms. Figure 17 presents data from the Chinn and Ito capital control index. Countries on the Arabian Peninsula have few capital controls and restrictions, which correlate with rapidly increasing levels of wealth. North African countries (with the exception of Egypt) have relatively closed capital markets. These countries correlate with relatively small markets for wealth management. Turkey represents the exception to the rule and has many capital market restrictions, which is not surprising given the three financial crises in the last 20 years. Opening up these markets can only help the wealthy and wealthy-to-be in these countries.

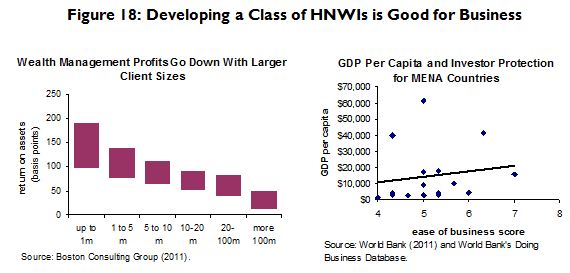

Developing a class of HNWIs would serve the asset managers as well. Figure 18 provides illustrations for reasons why international wealth management firms militate for banking, securities, and private sector reform in the MENA region. In terms of increasing margins, the graph on the left shows that smaller investors tend to pay more for services than UHNWIs. Clients bringing in up to $1 million pay roughly 1.5% in commissions and fees on their assets. Clients who bring in $100 million or more tend to pay roughly half of one percent. For the same $100 million, wealth managers should prefer (if we ignore costs) to serve many customers rather than one. On the macroeconomic side of the argument (and to repeat studies too numerous to cite here), countries which make doing business easy tend to see expanding levels and distributions of wealth. Once parliaments in the MENA region revise business legislation, the number and value of wealthy management clients will increase. Of course, the correlation is far from perfect — as the rich Qatar has the same ease of doing business rank as the much poorer per capita Morocco. Yet, the pattern seems clear.

Opening up these markets would also help foreign wealth management firms develop long-term relationships with their clients. The academic literature reaffirms what any practising wealth manager knows intuitively. Personal relationships affect their ability to accumulate assets more than other factors (like how profitably they manage portfolios or how efficient their bank office operations are). Cheng et al. (2010) put to the test the usual factors which McKinsey, the Economist Intelligence Unit, and other advisors to the wealth managers survey about. They find — using regression analysis — that personal and professional connections with the wealth manager statistically significantly correlate more than other factors (like the rate of return the wealth manager makes for his or her client or the wealth manager’s firm size). If the international wealth management firms want to capture a share of the future MENA wealth management market, they will need to locate in their markets.

The final reason why the big foreign wealth management firms should develop MENA markets consists in the diversification potential these markets offer the large international wealth managers. In a study of MENA markets, Lagoarde-Segot and Lucey (2007) find that portfolios that included MENA shares tended to have higher risk-adjusted returns than those without — because of the diversification potential of these shares. Even splitting the MENA into oil-producing and non-oil producing markets, Mansourfar and his co-authors (2010) also find significant diversification gains from investing in these countries’ firms. These gains mean — in simple language — that the big firms can get higher returns (or lower the risk they take for the same level of returns) by putting MENA shares in their portfolios. Having offices and local analysts in MENA countries will help these firms find the best assets — and help them to develop these assets at the same time.

Foreign entrants should resist the temptation to partner with government-owned banks. Kobeissi (2010) and Farazi et al. (2011) find (overall for the region) that government ownership exercises a negative influence on bank profits. In a wealth management context, partnering with state owned institutions poses an obvious danger — as many ultra-high-income-individuals seek to place funds abroad to escape local regulation or taxation or both. Several other authors repeat this conclusion — providing statistics for banking sectors with high levels of government ownership. For some of these countries, avoiding government participation will pose a challenge. In 2008, Farazi et al. find that the government has a 94% share in Libyan banks, 90% in Algeria, 69% in Syria, 57% in Egypt, 43% in Tunisia, 37% in Morocco, and 28% in the Gulf Co-operation Council countries overall. Yet, little government ownership does not guarantee a productive banking sector — as Yemen’s 13%, Jordan and Lebanon’s 0% government stake can attest to.

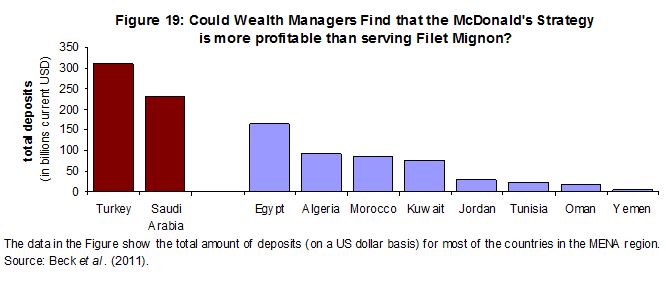

Current and potential entrants should also not overlook the potential profits of regular banking in the MENA region. If asset managers simply want to maximise assets under management, then the retail and commercial banking markets could be the best way to do that. Figure 19 shows the potential market size for gathering assets (in the form of the total number of deposits in various MENA country banks). The aspiring asset manager could gather over $250 billion in Egypt and Algeria. The convention wisdom — that wealth management and super-rich investors represent the “best” market segment to concentration on — still has yet to be proven.

Conclusions

Wealth management in the Middle East represents both a boon and a potential bust for local and international financial institutions. The future of wealth management in the Middle East will depend on whether policymakers and bankers can develop local wealth management services which grow local economies, and thus, increase the number and portfolios of affluent individuals. Policymakers will need to encourage local financial institutions to become more competitive by letting in foreign competition, changing banking and securities laws, and growing local companies whose share are worth buying. Foreign wealth managers need not fear the development of stronger local wealth management institutions and practices. They should use their bargaining power vis-à-vis Middle Eastern governments to make it easy to find and use locally-based wealth managers. They should also grow the market — by providing normal as well as private banking services. By offering higher rates of return to the affluent-to-be, these foreign wealth management firms can grow their market sizes and capture their share of the $800 billion already waiting for them.

References

Abbasoglu, Osman, Ahmet Aysan and Ali Gunes. (2007). Concentration, Competition, Efficiency and Profitability of the Turkish Banking Sector in the Post-Crises Period. Banks and Bank Systems 2(3).

Assaf, George, Carlos Barros and Roman Matousek. (2011). Technical efficiency in Saudi banks. Expert Systems with Applications 38(5): 5781–5786.

Becerra, Jorge, Peter Damisch, Bruce Holley, Monish Kumar, Matthias Naumann, Tjun Tang, and Anna Zakrzewski. (2011). Shaping a New Tomorrow: How to Capitalize on the Momentum of Change (Global Wealth 2011). Available online.

Beck, Thorsten, Aslı Demirguc-Kunt and Ross Levine. (2010). Financial Institutions and Markets across Countries and over Time: The Updated Financial Development and Structure Database. World Bank Economic Review 24 (1): 77-92.

Ben-Naceur, Sami, Ben-Khedhiri, Hichem, Barbara Casu. (2011). What Drives the Performance of Selected MENA Banks? A Meta-Frontier Analysis. IMF Working Paper No. 11/34. Available online.

Boston Consulting Group. available online.

Cheng, Jao-Hong, Huei-Ping Chen, Chih-Ming Lee, Yueh-Hsiu Liao and Shu-Nu Chan. (2010). Theoretical Perspectives on the Outsourcing Delegate in Personal Wealth Management Contemporary Management Research 6(2): 111-124. Available online.

Chinn, Menzie and Hiro Ito. (2008). A New Measure of Financial Openness. Journal of Comparative Policy Analysis 10(3): 309 - 322.

Credit Suisse. (2010). Global Wealth Databook.

Eljelly, Abuzar. (2009). Ownership and Firm Performance: The Experience Of Saudi Arabia’s Emerging Economy. International Business & Economics Research Journal Volume 8(8). Available online.

Farazi, Subika, Erik Feyen and Roberto Rocha. (2011). Bank Ownership and Performance in the Middle East and North Africa Region. World Bank Policy Research Working Paper 5620. Available online.

Haddad Mahmoud, and Sam Hakim. (2010). Have Foreign Banks Contributed to the Spread of the Global Financial Crisis to Saudi Arabia? Economic Research Forum Working Paper 537. Available online.

Hall, Peter and David Soskice. (2001). Varieties of Capitalism: The Institutional Foundations of Comparative Advantage. Oxford.

Hasan, Maher and Jemma Dridi. (2010). The Effects of the Global Crisis on Islamic and Conventional Banks: A Comparative Study. IMF Working Paper No. 10/201.

Kobeissi, Nada and Xian Sun. (2010). Ownership Structure and Bank Performance: Evidence from the Middle East and North Africa Region. Comparative Economic Studies 52, 287–323.

Lagoarde-Segot Thomas and Brian Lucey. (2007). International portfolio diversification: Is there a role for the Middle East and North Africa? Journal of Multinational Financial Management 17(5): 401-416.

Mako, William and Diego Sourrouille. (2010). Investment Funds in MENA. Paper prepared for the World Bank Flagship Publication. Available online.

Mansourfar, Gholamreza, Mohamad Shamsher and Taufiq Hassan. (2010). The Behavior of MENA Oil and Non-oil Producing Countries in International Portfolio Optimization

The Quarterly Review of Economics and Finance 50(4): 415-423.

Maude, David. (2006). Global Private Banking and Wealth Management. Wiley Finance.

Merrill Lynch.and Cap-gemini.(various years). World Wealth Report.

Skolkovo Emerging Markets Briefs series (2012). Available online.

Steiner, Christian. (2010). An overestimated relationship? Violent political unrest and tourism foreign direct investment in the Middle East. International Journal of Tourism Research 12(6): 726–738.

VRL. (2010). Middle Eastern Wealth Management.

Yildirim, Canan. (2010). Cherry Picking or Driving Out Bad Management: Foreign Acquisitions in Turkish Banking. Economic Research Forum Working Paper 568.

Appendix I: Local laws on their effect on the foreign wealth management industry

The following presents a sample of investment laws from the region. We show the law and the reasons why specific provision encumbers the growth of a domestic wealth management industry.[2]We make no guarantees that the laws we have reviewed represent legislation or regulation in effect at the time we reviewed them.

|

The Law |

Comments |

|

Algeria |

|

|

Ordinance 01-03 of 20 August 2001 on Investment Development provides the basic tax and customs incentives defined in investment promotion laws across the MENA region. |

|

|

Banking Law 90-10 of 10 April 10 1990 places primary responsibility for regulating the banking sector with the Bank of Algeria. Few other laws are available — and available evidence suggests that the Bank of Algeria governor decides which banks may operate in Algeria. |

|

|

Egypt |

|

|

Presidential Decree No. 187 of 1993 Issuing the Executive Regulations of the Banks and Credit Law requires foreign banks (or banks with more than 50% ownership) to guarantee deposits in case of bank failure (art. 4.6) and information about foreigners working in the branches in Egypt. |

|

|

Law No. 88 of 2003 Promulgating the Law of the Central Bank, the Banking Sector and Money authorises foreign banks to operate (article 35). The law requires these banks to join the national self-regulating organisation and be subject to national oversight (article 54). Article 111 guarantees the right to transact and deal in foreign currencies. |

|

|

The Investment Law No. 8 of 1997 represents Egypt’s version of legislation offering investors tax incentives, customs exemptions, and protections against appropriation. |

|

|

Jordan |

|

|

Banking Law No. 28 of 2000 provides a liberal regime for the regulation of foreign banks operating in Jordan. Article 11 lays out the procedures for the licensing of foreign banks. Securities Law No. 76 of 2002 looks like similar laws in the US and Europe. Unlike the other countries in the region, Jordanian banking and securities law seems relatively unremarkable. |

|

|

Lebanon |

|

|

Article 1 of the Basic Decision No 7074 of the Bank of Lebanon Relating to Collective Investment Schemes explicitly forbids any foreign wealth management or bank from soliciting for funds in Lebanon without prior consent from the Bank’s Board. The rest of the decision describes the conduct of investment promotion activities in the country. |

|

|

Law 360 of 2001 Encouraging Investments in Lebanon outlines many of the exemptions, tax incentives, and other enticements given to foreign investors. |

|

|

Law 234 of 10 June 10 2000 On Regulating the Financial Intermediation Profession restricts financial activities to those licensed by the (Central) Bank of Lebanon. The law sets forth restrictions on the amount of foreign ownership (article 5) and generally sets forth the conditions for foreign financial institutions wishing to operate in Lebanon. Other relevant legislation includes Law 706 of 2005 on Collective Investment Schemes in Securities and Other Financial Instruments and Law 99 of 1991 Regarding Lebanese and Foreign Banks. |

|

|

Morocco |

|

|

Law 18 of 1995 Establishing an Investment Charter aims to replace the nine investment laws in force. The Charter (of uncertain legal and regulatory validity and status) grants the usual benefits to foreign investors in the areas of tax and customs. |

|

|

Law 34 of 2003 on Credit and Financial Institutions represents an unremarkable legislative instrument outlining the organisation and structure of the banking sector. |

|

|

Law No. 58-90 on Off-shore Financial Markets basically creates a financial free zone (much as the UAE has done) with its own rules with regard to transacting with foreign financial institutions. Foreign banks may operate with few rules in Tangiers. |

|

|

Oman |

|

|

Master Circular BM-997 on Lendings to Non-Residents and Placements of Bank Funds Abroad of 2006 restricts the placement of bank funds abroad of foreign bank branches operating in Oman. Banks are allowed to keep 20% of net worth in foreign currency (point 6.1). Banks should (as per point 6.6) report any placements abroad within the following month. Royal Decree 102/94 Law on the Issuing the Foreign Capital Investment limits foreign ownership of companies to 49% (rising to 65% with a recommendation from the Foreign Capital Investment Committee and the approval of the Minister of Commerce and Industry). Capital participation may rise to 100% for small projects of special development interest. These restrictions may be waived by special agreement of the Government. Article 4 requires licensing of foreign investment. Article 8 defines special industries. The law also gives dispensations of customs duties. |

|

|

The Instruction for Establishment of Omani Companies Subject to Commercial Companies Law and Foreign Business and Investment Law establishes limits on the amount of foreign capital (point 6) and the types of sectors foreigners may participate in (point 7). The instruction also requires 5 years relevant previous commercial experience and the explicit consent of relevant government agencies (point 8). |

|

|

Saudi Arabia |

|

|

Saudi Securities and Investment Fund law closely resembles international norms. Banking Control Law of June 1966 allows foreign banks to operate in the Kingdom, subject to licensing. |

|

|

Saudi Arabian Monetary Agency Regulations for Investment Funds and Collective Investment Schemes Circular of 1993 describe restrictions on both foreign financial institutions operating in Saudi Arabia and Saudi institutions wishing to operate abroad. Point 1 of the circular forbids foreign financial institutions from offering banking services in the Kingdom. Point 3 specifically requires Monetary Agency to approve in advance any monies sent abroad. |

|

|

The Foreign Investment Act of April 2000 stipulates that General Investment Authority license Foreign Capital Investment (as defined in article 2 of the Law). Foreign investors possess the same general rights — with some exceptions including restrictions on real estate investment (article 8). Executive Rules of the Foreign Investment Act refers to firms wholly-owned by foreign investors (article 4.2), outlines benefits and incentives given to foreign investors (article 5), and principally describes licensing procedures (articles 6-19). |

|

|

Syrian Arab Republic |

|

|

Investment Promotion Law No. 10 (as amended by Legislative Decree No. 7 of 13 May 2000) outlines the rights of the foreign investor. The law covers many of the basic rights we take for granted in the West, including the usual guarantees against appropriation (article 3), right of abode (article 4), and tax incentives (outlined in Chapter 2). Funds may be remitted annually (after settling taxes). Amendments allow company management to decide company wages, appointments, and other HR decisions. |

|

|

Tunisia |

|

|

Law 2001-65 of the 10th July 2001 on Credit Agencies establishes a system of mutual recognition for foreign investment agencies and banks registered in Tunisia (article 12). |

|

|

Law 85-108 of the 6th December 1985 on Promoting Banking and Financial Organisations working principally with non-residents guarantees the rights of foreign financial organisations without the discriminations found in much MENA law. |

|

|

Law No. 93-120 Promulgating the Investment Incentives Code establishes incentives for investing in 14 sectors of the Tunisian economy (such as agricultural, manufacturing and other “productive” activities). In general, the law sets up a complex system of benefits. Article 3 restricts foreign participation to a 50% stake in the local company and licensing by the Higher Investment Commission. Article 12 allows foreign companies to opt-out of the Tunisian pension contribution scheme. |

|

|

Turkey |

|

|

Banking Law No. 5411 and Banks Act No. 4389 provide unremarkable regulation of Turkish banks. |

|

|

Law No. 4875 on Foreign Direct Investment provides the general framework for guaranteeing foreign investors the basic rights found in similar documents across the region (such as national treatment and freedom from appropriation). Article 34 of the Law 2499 of 1981 on Capital Market grants the Capital Market Board the right to establish the principles for regulating foreign financial institutions. |

|

|

Free Trade Zones Act dated 6 June 1985 in theory provides the same kind of inducements like Tangiers and Dubai to set up special banking zones. However, the government has not allowed any particular financial free zones at this time. |

|

|

United Arab Emirates |

|

Federal Law 8 of 2004 Regarding the Financial Free Zones creates areas which are exempt of the generally higher level of regulations. Article 2 makes these zones completely self-regulating. Law No. 12 of 2004 on the Judicial Authority at Dubai International Financial Centre represents an example of a specific zone created under this legal framework. |

|

The Federal Act No. 18 of 1981 Concerning Organizing Trade Agencies and the Commercial Companies Law No. 8 of 1984 forbid foreigners from owning more than 49% of a company (including an investment company) and require the use of an agent to engage in foreign trade. |

|

Yemen |

|

Law no 38 of 1998 on Commercial Banks represents a pedestrian banking law. Article 5 requires license from Central Bank to engage in banking activities. Article 10 defines restrictions on bank capital management, mergers and other activity. The law gives effect to various provisions in the Islamic Banking Law which restrict banks’ investment activities (article 20 and 21). |

|

The Investment Law No. 22 of 2002 provides a highly detailed account of the rights and obligations of foreign investment projects operated in Yemen. Article 9 requires 15% “preference” price reduction. Article 13 allows for nationalization if in the public interest. Article 17 calls for a pro-Yemeni bias in employment. |

|

Law No. 23 of 1997 on Arrangement of Agencies, Branches of Companies and Foreign Trade Houses represents a highly restrictive piece of legislation which makes the practice of foreign investment and banking extremely difficult. Some examples include Article 4 requires Yemenis only to hold capital in the company. Article 6 requires authorization from “the competent ministry in advance.” The law also requires review of the agency contract with the foreign financial institution. Article 9 requires the submission of fees. Article 17 prevents imports unless approved in advance. |

Source: Author and World Bank Doing Business Law Library.

Note: Iraq omitted due to likely changes in laws. Dates on Saudi laws have been converted into equivalent Gregorian calendar dates.

[2] Doing Business Law Library, available online. We sorted by Banking and Credit Laws, Commercial and Company Laws, and Securities Laws.

The Middle East Institute (MEI) is an independent, non-partisan, non-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.