The MENA Energy Recap is a quarterly review of key energy developments that took place in the region from April through June of 2025 and what they signal in the months ahead. The Recap views these developments through the lens of policy and strategy, energy security, and markets.

Q2-25 in Brief

In the inaugural MENA Energy Recap for Q1, the first three months of 2025 were characterized as “a period of scene setting for what looks likely to be a highly volatile year in both markets and geopolitics,” and events in Q2 have hardly disappointed. The 12-day war between Israel and Iran sent oil prices spiking into the $80 per barrel (bbl) range, but the geopolitical risk premium it created came and went in the span of a single month, with the focus now returning to supply and demand fundamentals as well as the potential impact of what looks increasingly like another flare-up in US President Donald Trump’s trade wars.

Geopolitical risks appeared to pose more of a threat to energy supplies within the Middle East than they did to energy exports from the Gulf region, with key natural gas supplies shut in and representing what would ultimately be the most serious energy-related disruption of the conflict. Prior to the outbreak of war, though, it became increasingly clear that the list of countries in the Middle East and North Africa experiencing temporary energy shortages or having to turn to external markets to shore up domestic shortfalls would grow this summer, highlighting a worrying seasonal trend that shows little sign of abating. In wealthier countries, energy security continues to be bolstered by the expansion of renewable power capacity, pointing to an ever-wider divergence between net exporters and states that must increasingly take extra measures to shore up energy security with ever scarcer resources. Yet amid both predictable and unforeseeable regional volatility in Q2, there are currently few deterrents to increased energy investment in the Middle East, and state-owned firms appear set to continue to invest outside of the region as well, even in the face of an uncertain and potentially unfavorable period in oil markets.

Policy and Strategy: Investments Flows as Gulf NOC Capex Holds Steady

- President Trump’s first major overseas trip to the Gulf region in May was, prior to the June Israel-Iran war, viewed as a leading indicator of the trajectory of US-Middle East relations in the second Trump administration. While bilateral ties between the United States and the Gulf countries are becoming increasingly diversified across a range of issues outside of the traditional areas of energy and security, key agreements bolstering the bilateral flow of oil and gas investments were announced during the trip.

- As these relationships evolve and the US imports incrementally fewer barrels of crude from the Gulf region, the focus of energy ties is shifting toward bilateral investment, with the US becoming an important investment destination for Gulf national oil companies (NOCs) and their ongoing efforts to grow their global portfolios.

- This will be an important dynamic if Gulf NOCs invest beyond major liquefied natural gas (LNG) projects and petrochemicals assets. This is particularly relevant since Gulf firms appear poised to maintain their capital expenditures (capex) through a period of relatively lower prices and economic uncertainty as US firms cut guidance and lower expectations of production growth.

Outlook: Unlike other oil- and gas-sector firms, Gulf NOCs appear largely intent on spending through the current downturn, driving strategic domestic projects toward completion and continuing to grow their portfolio of overseas assets. Most notable among these were the announcement by Abu Dhabi National Oil Company (ADNOC) that its XRG subsidiary would partner with United Arab Emirates state holding firm ADQ and private equity firm Carlyle to acquire Australia’s Santos and its portfolio of LNG assets. Of lesser note was QatarEnergy’s entry into Algeria alongside TotalEnergies, where the two will split a 49% stake in the Ahara license. After President Trump’s visit to the Gulf in May, Saudi Aramco signaled its intent to expand its wholly owned Motiva refinery, the largest in the US, to include an integrated petrochemical facility.

Other agreements, such as that indicating ADNOC’s interest in building carbon capture and storage (CCS) facilities in the US, further boost Gulf NOCs’ visibility as increasingly prolific investors in the global energy industry. While it was clear that these firms viewed the US as an important part of their portfolios before Trump’s reelection, his drive to attract foreign investors and Gulf capitals’ desire to remain close to the Trump White House have only increased the incentive to build on this trend. The US may no longer be a key market for energy exports from the Gulf, but it is an increasingly important investment destination for Gulf energy firms, with the UAE seeking to grow its portfolio of US energy assets to $440 billion by 2035.

Regional volatility that occurred later in the quarter is unlikely to reduce the attractiveness of the Middle East for major US energy firms, the presence of which is increasingly important to oil and gas growth plans. Perhaps the strongest example of this is the entry of US shale player EOG Resources into the Abu Dhabi upstream sector. Partnering with international firms has been a crucial way for Gulf NOCs to expand their access to key energy technologies and hone their expertise in value-added processes. As the development of unconventional natural gas resources is a priority for ADNOC in support of the UAE’s goal of reaching gas self-sufficiency by 2030, the first entry of a major US shale specialist suggests that ADNOC is likely to get increasingly serious about expanding its expertise in unconventional resources development — something it has also signaled its intent to do by moving up the American natural gas value chain and making investments in the US upstream sector.

US oil and gas majors, as well as independent players like EOG, have long been active on a global scale, and there is no sign that this is likely to change in either the near or long term. While the longstanding framework of “energy for security” for US-Gulf ties may be in its twilight years, a different sort of bilateral energy relationship may just be getting started.

Energy Security: Few Improvements in Seasonal Energy Shortfalls This Year

- In recent years, Egypt and Iraq have consistently experienced summer energy shortages when seasonal demand for electricity peaks due to soaring air conditioner use.

- As time has gone by, however, other regional states have also begun to experience power shortfalls in the heat of summer, including Iran and Kuwait. In 2025, Bahrain will import its first LNG cargoes in order to fill a supply gap left by declines in domestic output.

- Natural gas shortages are behind summer power outages in most countries, with the exception of Kuwait, which has maxed out its power generation capacity. Supply-side shortfalls crop up for a variety of reasons, but the long-term trend highlighted by this increasingly common occurrence is continued demand growth from the region.

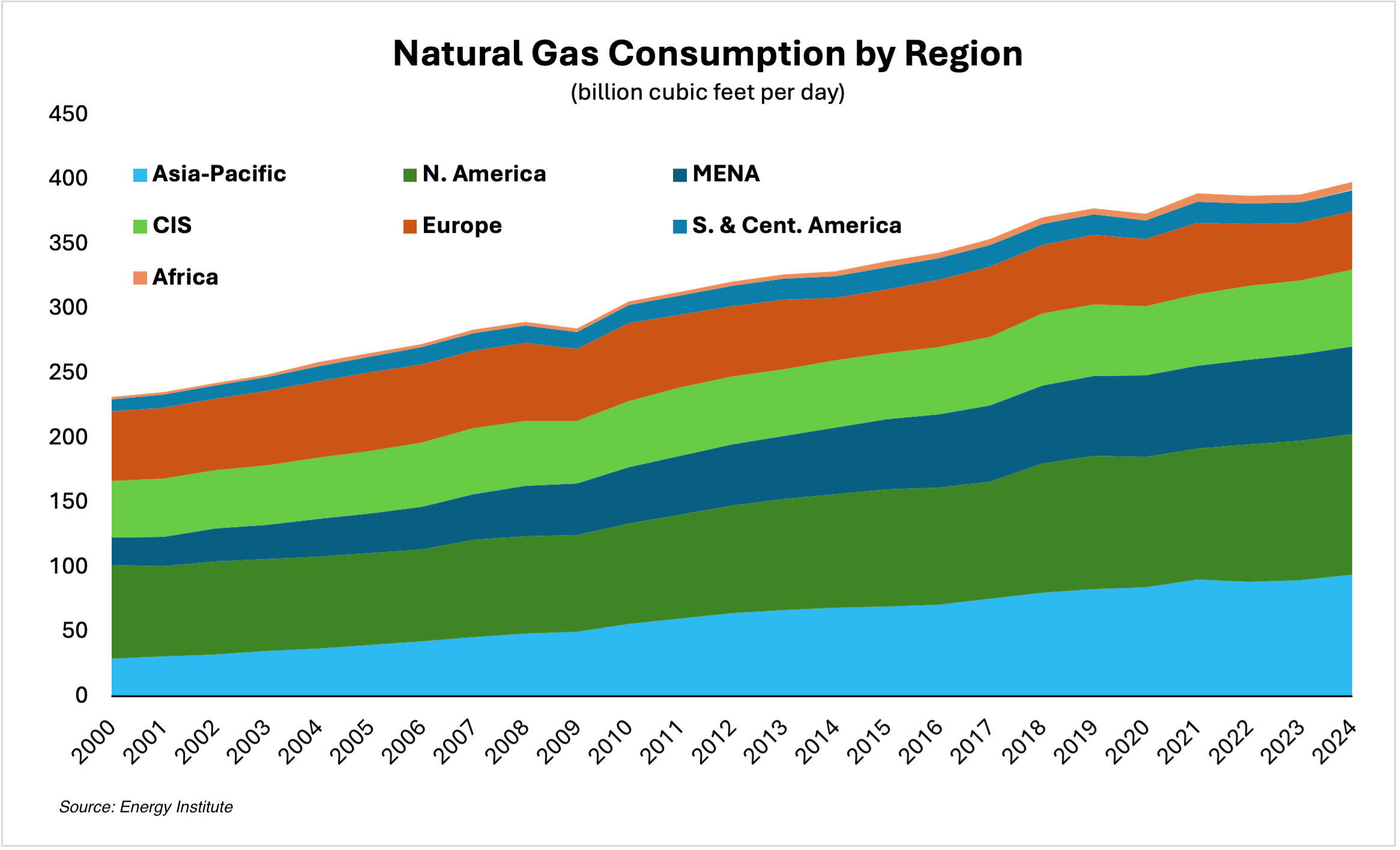

Outlook: Natural gas consumption in the MENA region accounted for around 17.5% of the global total in 2024, according to new figures from the Energy Institute. This makes MENA the third-largest consumer by region, surpassed only by North America and Asia-Pacific. This trend has been supported by a number of factors, most notably an abundance of local resources and subsidized energy consumption, as well as population growth. Continued increases in gas demand suggest its expansion could reach as high as 24% over the course of the current decade.

While a number of wealthier countries across the region are working to boost gas production, often in the name of shoring up domestic energy security, other countries such as Egypt, Iraq, Iran, and Bahrain lack the resource base to do so or have fallen behind. While Egypt is able to import pipeline gas from Israel, Kuwait sources most of its LNG cargoes from nearby Qatar, and the UAE uses the Dolphin Pipeline to source around 20% of its gas requirements from Qatar, these represent the exception rather than the rule when it comes to the regional energy trade. Looking ahead, these exceptions appear likely to remain few in number. It is likely no coincidence that the agreement for pipeline gas deliveries from Qatar expires in 2032, just two years after the UAE’s target for reaching gas self-sufficiency. While Bahrain has reportedly sought a pipeline linkage to Saudi Arabia through which it could import low-cost gas, this idea does not appear to have strong momentum. Gas-rich countries have clearly expressed more interest in using incremental volumes for higher value applications, such as supporting energy-intensive artificial intelligence (AI) processes in the case of Saudi Arabia or expanding LNG exports in the case of Qatar. In either instance, using gas production to support these goals generates value for producer countries that is exponentially higher than agreeing to sell pipeline volumes to neighboring countries at low prices.

Accordingly, policymakers should consider that regional integration of the energy trade has few successes to which it can point. While examples in the Gulf are extremely limited, attempts to integrate gas markets in the Eastern Mediterranean have stalled for years despite the prospect of the region establishing itself as a major new supplier to European markets in the aftermath of the 2022 Russia-Ukraine war. For those in the MENA region that face gas and power shortfalls, integration with global gas markets and an accelerated buildout of renewable power generation capacity may offer greater stability than the often ill-fated attempts at developing a more regional gas and power market. Development of LNG import infrastructure does expose importers to global gas market volatility but also prevents one country from being bound too closely to another via pipeline imports that can be cut off due to political, security, or other issues. This also presents an opportunity for the US to strengthen ties with key partners in the region like Kuwait, Egypt, and now Bahrain, all of which are LNG importers. Deliveries of US LNG cargoes to the Middle East leapt in 2024, rising over 300% from 2023, and look set for another sizeable increase this year.

Additionally, nearly all countries in the region have strong renewable power potential. Providing support to accelerate existing renewable projects or develop new ones will help countries to establish a degree of “energy sovereignty” that will not leave them reliant on imports from neighboring countries and offer a hedge against volatility in global energy markets. Egypt has made considerable progress in this regard and maintains an impressive portfolio of upcoming renewable energy projects, but countries like Iraq and Kuwait have fallen further behind. Washington should revisit recent policy moves that are largely hostile toward support for the proliferation of renewable energy at home and abroad. This approach will cede potential avenues for cooperation with both the US government and US firms to strategic rivals such as China, to whom even lagging renewable energy developers have been turning for help. Iraq is a prime example; the Trump administration’s dim view of renewables is unlikely to take priority over the need to help wean Baghdad off of its dependence on imports of Iranian natural gas.

Energy Security: War Highlights Ever-Present Risks in an Energy-Abundant Region

- Twelve days of intense fighting between Israel and Iran that began this past June saw risks to energy production and shipping from the Gulf region soar. While the conflict ultimately ended without any such disruption, it underscored that there are still significant potential threats to energy production in the region.

- However, markets reacted in a relatively muted fashion when compared with other, major geopolitical events in recent history, such as the 2022 Russian invasion of Ukraine and the subsequent price spike that sent oil prices past $120/bbl.

- The real effects were felt by intra-regional energy trade in the wider MENA region amid efforts to mitigate the potential risks to energy infrastructure. This was painfully clear in Egypt and Jordan, where Israel’s decision to shut down two of its largest offshore gas fields deprived its neighbors of critical pipeline imports.

Outlook: One of the most significant takeaways from the Iran-Israel war as it pertains to the energy sector is that fighting in the region may represent less of a risk to global energy security than it does to the security of supply for those in the region. This was underscored by Israel’s attack on natural gas processing facilities linked to Phase 14 of Iran’s highly critical South Pars project. While not a major outlet for Iranian oil exports, production from South Pars services 75% of Iran’s domestic gas demand. The intensely critical nature of South Pars production initially made it seem as though Israel’s targeting of the energy sector could grow much more aggressive than it ultimately did. A major loss of domestic natural gas supply in Iran would not only have been catastrophic for its energy security but also disastrous for neighboring Iraq, which is highly dependent on Iranian imports to make up for its own supply shortfall, particularly in the summer months when demand for air conditioning use soars.

Yet the “energy escalation” did not lead to the targeting of major energy production assets in a manner that would impact global markets. It did, however, result in Iranian retaliation that knocked Israel’s largest refinery offline. Still, the most significant impact to the regional energy trade was the shut-in of Israel’s Leviathan and Karish gas fields, which together account for 77% of total Israeli production, and resulted in the aforementioned halt to exports. Such shut-ins are not without precedent, and have taken place several times since 2021, albeit on a smaller scale. In this instance, the stop to production necessitated a simultaneous halt of exports to Egypt and Jordan, both of which are highly dependent on Israeli pipeline volumes. Each holds the ability to source LNG cargoes from the spot market (referring to cargoes bought for immediate delivery and not as part of a long-term supply agreement) via floating storage and regasification units (FSRUs), but doing so is considerably more expensive than relying on pipeline volumes. Still, the ability to tap LNG markets likely meant the difference between keeping the lights on and much more acute energy shortages, raising longer-term questions about the degree to which greater regional integration of energy markets supports energy security or leaves states that are highly dependent on imports more exposed to potential outages.

Policy and Strategy, Energy Security: Renewables Growth Keeps Pace Across Region

- As momentum behind decarbonization and a shift to less carbon-intensive forms of energy wanes in the US and parts of Europe, the MENA region has continued to move forward without signaling that efforts to diversify energy supplies are slowing down.

- Morocco is the undisputed regional leader, with 38% of its total generation capacity coming from renewable sources in 2024, although its overall generation capacity is smaller than that of many others in the region. The Gulf states and Egypt look set to continue expanding their renewable power capacity, helping to offset the use of hydrocarbons in the power generation sector to either free them up for export or, in the case of Egypt, to reduce the need for more expensive imports.

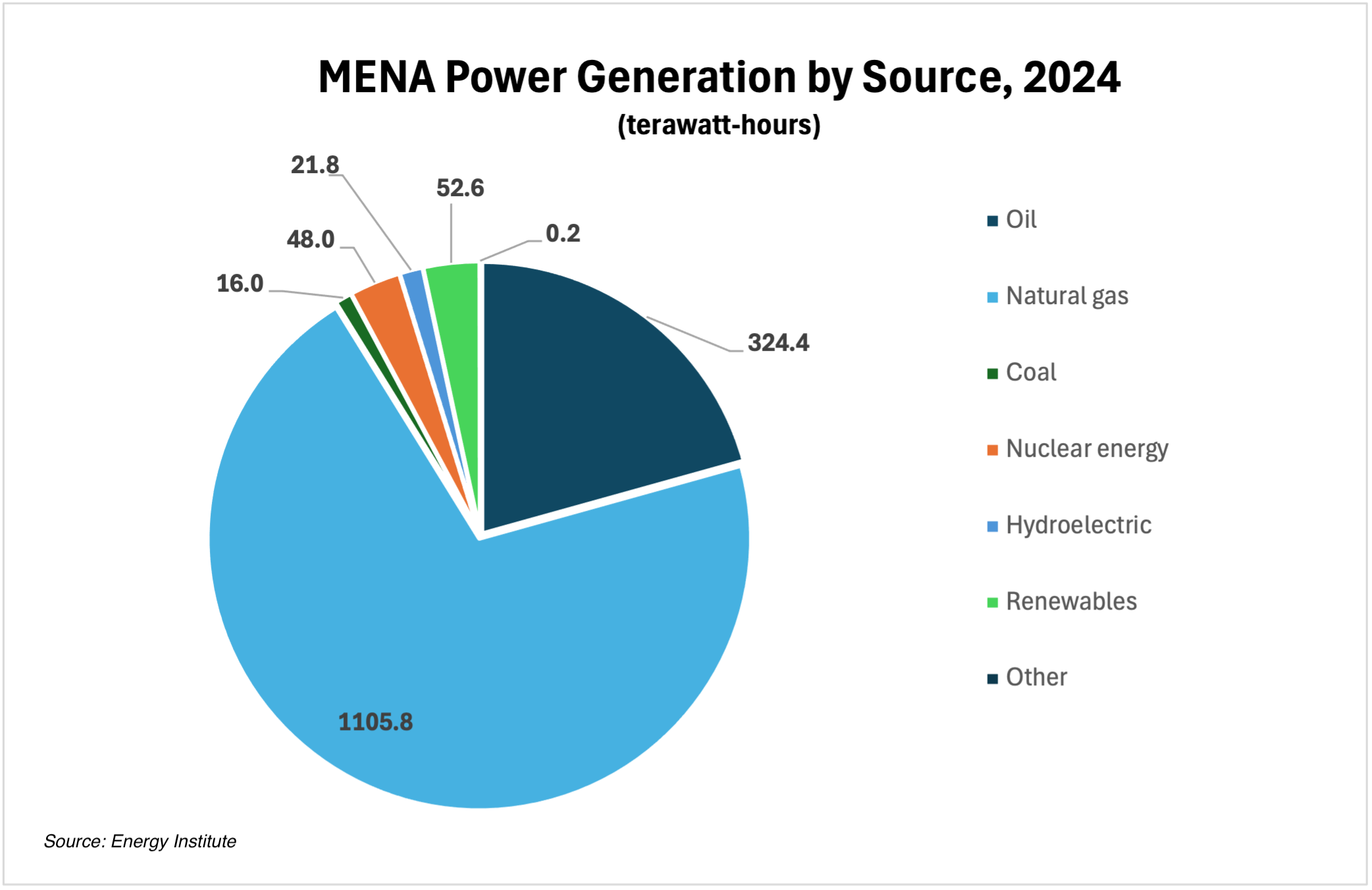

- Still, natural gas looks set to remain the power generation fuel of choice for the remainder of the 2020s. A number of countries across the region boast renewables targets for the year 2030, and while many of these will likely be achieved, the need to ramp up domestic gas production or procure external supplies is only likely to continue growing.

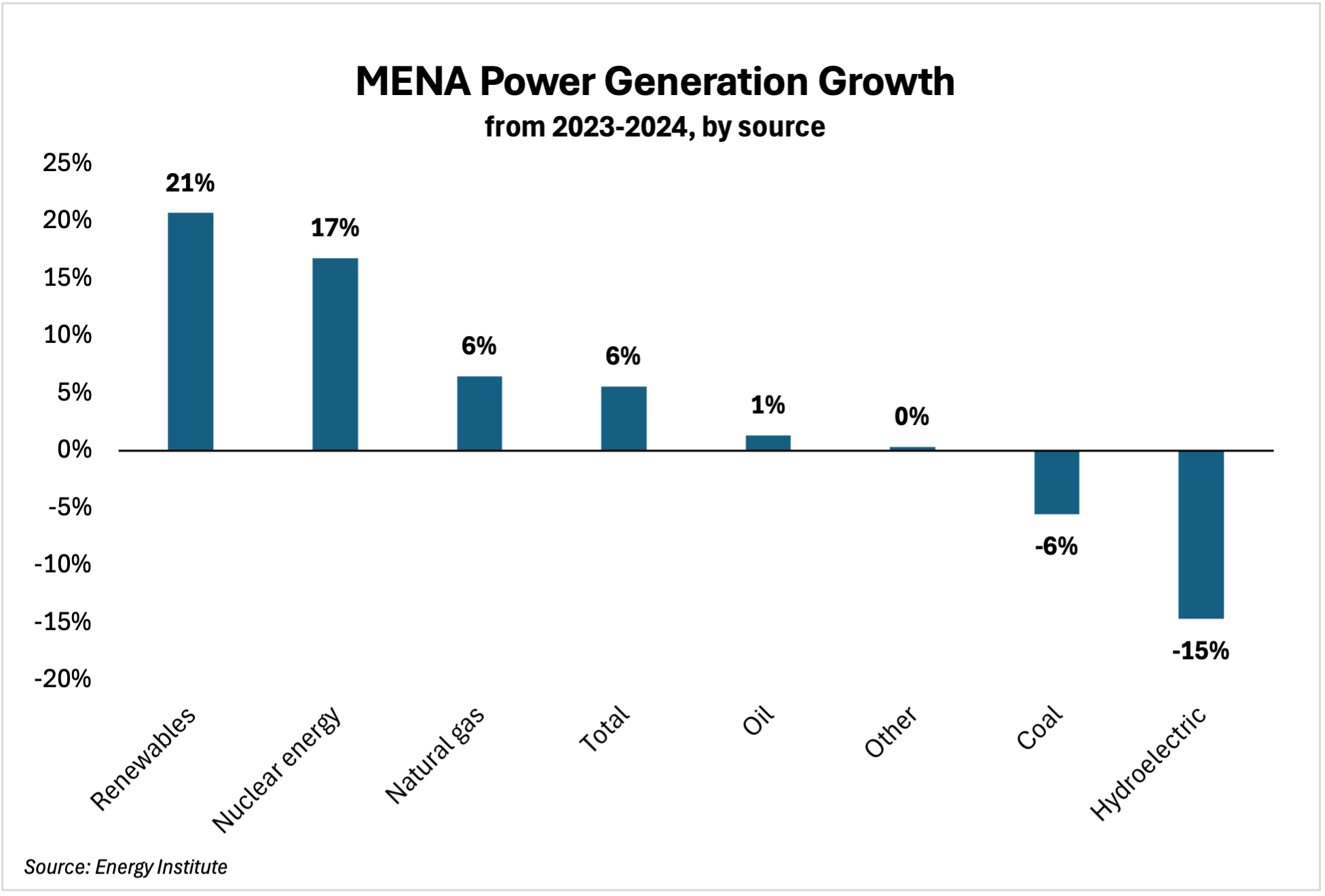

Outlook: Progress in developing the renewable energy supply across the MENA region remains limited to a handful of countries that have been able to advance major buildouts of new capacity, mostly in the form of solar photovoltaics (PV), but in some instances this has also included wind. New data from the Energy Institute and the International Renewable Energy Agency (IRENA) shows that growth in both capacity and total generation sustained momentum in 2024; renewable energy now accounts for 10.8% of installed power generation capacity in the region, while total generation rose to 3.35%. Renewables make up a proportionally greater share of the power mix when hydroelectric power is included, yet most of this is legacy capacity, and hydroelectric generation is not a component of existing strategies to expand more cost-effective solar and wind capacity.

While this data points to a long road ahead for renewables to eventually displace other sources of power generation in the region, rather than just meeting new power demand growth, low percentages are not necessarily a reason for pessimism. Renewable generation posted the most growth from 2023-24, with nuclear slightly behind at 17%.

Capacity growth in Oman, Saudi Arabia, and the UAE has accelerated rapidly since the beginning of the decade, and the Saudi renewable sector may soon become the region’s largest with Riyadh’s plans to tender 20 gigawatts (GW) of new renewable energy projects every year until 2030. A number of countries in the region have seen renewables targets come and go in the past, but the fact that many of these projects support much more critical, strategic national initiatives than they had in the past is a reason to expect that the current momentum will continue to deliver results. Still, natural gas accounts for a huge share of the region’s power generation mix, whether it is sourced from domestic output, or imported via pipeline or LNG. Yet as the region’s overall energy demand continues to grow, renewables and to a somewhat lesser extent nuclear power are going to play an increasingly prominent role in the generation mix, coming largely at the expense of oil- and coal-fired power generation.

Markets: OPEC+’s Big, Beautiful Barrels

- The supply additions by the group of 12 Organization of Petroleum Exporting Countries (OPEC) plus 10 non-OPEC oil-producing nations (OPEC+) through 2025 continue to surpass expectations, with the latest decision to add 548,000 barrels per day (bpd) from August onward catching by surprise even those expecting continued additions of 411,000 bpd through at least September. The group is now on track to unwind its voluntary cuts from 2024 even sooner than anticipated.

- OPEC cites bullish oil market views as a component of its decision, anticipating close to 1.3 million bpd in demand growth for 2025. In reality, its strategy is more likely to be motivated by a desire to recapture market share and reinforce cohesion among key group members.

- Additionally, the long-term impact of its decision may be a suppression of non-OPEC+ supply growth, which until recently has been sufficient to meet new oil demand growth while OPEC+ had kept over 5.5 million bpd in spare capacity sitting idle. No longer willing to sacrifice market share to support prices, group strategy now deviates sharply from the approach it took in the post-COVID recovery period.

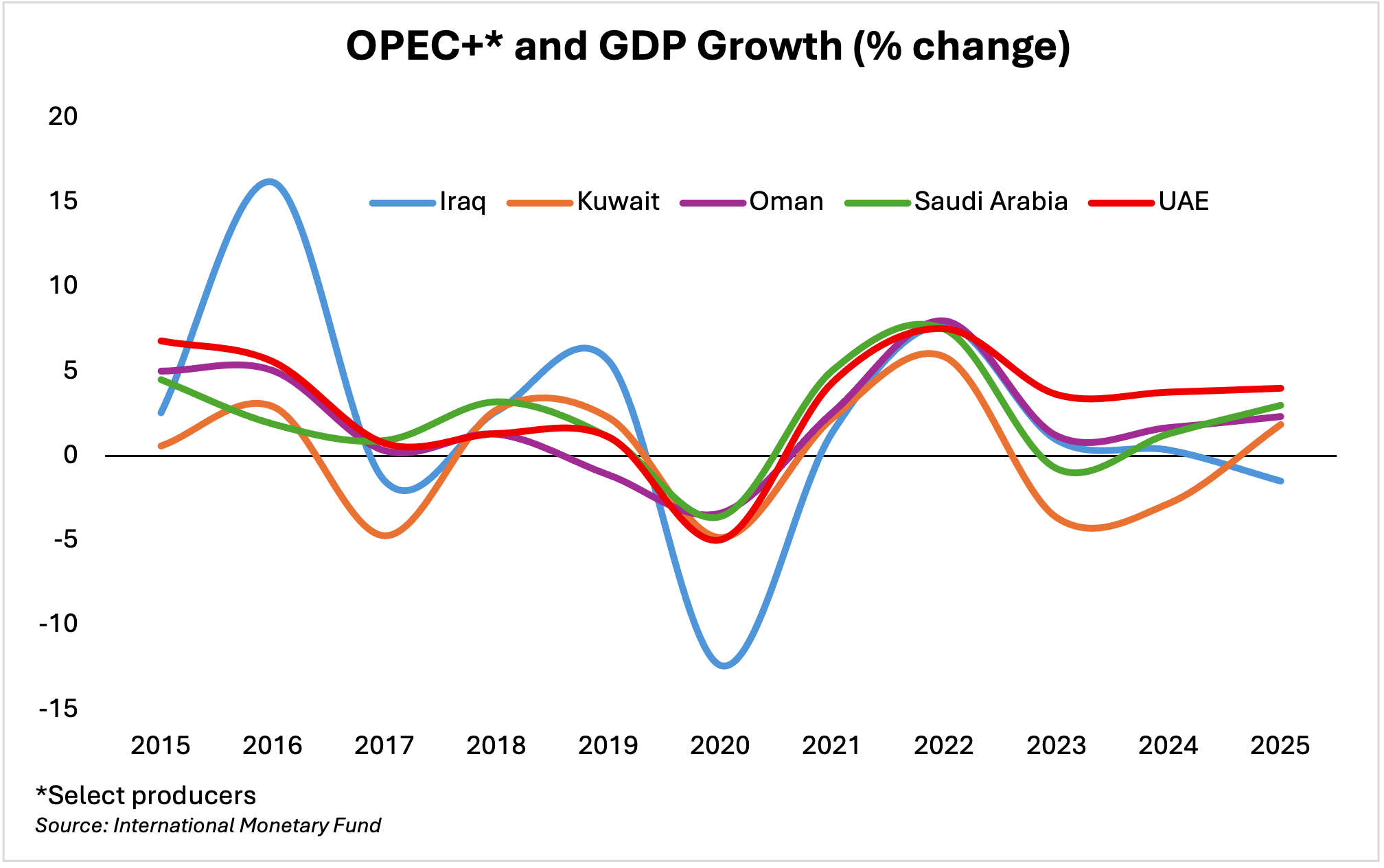

Outlook: Accelerated supply additions from OPEC+ continue to surprise some market watchers by bringing more supply back to market at a time when prices are averaging lower than they have in previous years, and economic growth is overshadowed by uncertainty around further ruptures in global trade relations with the US, particularly between Washington and Beijing. Yet when considered against a longer-term view, the group’s policy is easier to understand, even if some would disagree with its approach. The group sits on three layers of deep cuts that have been in place since 2022, with the most recent tranche of voluntary cuts being the one it is currently racing to unwind. This “third layer” was originally scheduled for unwinding in Q2 2024 but was postponed for a full year, testing the patience of quota-compliant group members while output constraints were virtually being ignored by others, and raising serious concerns about the group’s loss of market share to non-OPEC+ producers.

When weighed against these concerns, the decision to increase production across the group makes significantly more sense. OPEC and OPEC+ have historically been viewed as acting in defense of key price bands, but several major producers underwent economic contractions or lower GDP growth after the imposition of these deep cuts in 2022, and results were no better in 2024. This clearly prompted a rethink of the group’s strategy in which price is no longer a central consideration, even if it is still an important one. In addition to this, President Trump’s desire to keep energy prices low provides an arguably historic opportunity to ramp up production and squeeze higher-cost US shale producers without risking tension between major OPEC states (particularly those in the Gulf) and Washington. Yet much of the group’s trajectory for the rest of 2025, and indeed into 2026, may well be determined by US policy if global economic growth underperforms due to the imposition of US tariffs, which in early Q3 appear to be making a potential comeback. OPEC’s internal, ever-bullish outlook for demand growth may cite a range of very real factors underpinning the group’s optimism, but it will have little more success than any other forecaster in predicting how a second rollout of post-“Liberation Day” tariffs may impact global oil demand.

Outlook for Q3-25

Despite the immense volatility felt in the energy sector and beyond when Israel and Iran went to war in June, the outlook for oil- and gas-dependent countries in the region will largely return to US policy in Q3, reinforcing the assertion in the Recap’s inaugural Q1 issue that the “Trump factor” will continue to loom large for Gulf producers in 2025. While there was considerable focus on the potential oil market impact of a renewed nuclear agreement between the US and Iran, events in Q1 were largely centered on US trade policy and Trump’s aggressive use of tariffs to secure new trade agreements. As Q3 gets underway, it is already apparent that this issue will return to center stage in the coming weeks, months, and potentially even years.

Yet trends continuing in Q2 also underscored the limit to which US policy has the ability to impact high-level strategy in the Middle East energy sector. While domestic US policy has seriously downgraded key priorities from the Biden administration around low-carbon energy resources, which has in turn had a ripple effect throughout a number of regions, the Middle East is largely unmoved by this policy shift. Regional states able to do so are keen to produce more energy of all forms, be it from their own domestic oil and gas resource base, strong renewable power potential, or pursuit of nuclear power (although the latter hardly deviates from the Trump administration’s own priorities). The most tangible impact the White House’s shift in energy policy may yield is a slowdown in US-based renewable energy investment, which thus far has been led by the UAE’s Masdar. Yet where this may come at a cost to Masdar’s portfolio, other Gulf firms may stand to benefit — ADNOC’s signature of an agreement to explore a direct air capture (DAC) facility, a form of CCS technology, with US oil firm Occidental Petroleum is likely to receive more help than hindrance with the passage of Trump’s signature “One Big Beautiful Bill” (OBBB). DAC is an expensive technology, and the OBBB expands 45Q tax credits, which are designed to support CCS development. CCS technology is already a priority for leading Gulf NOCs, and they will in theory receive further incentives to invest in US-based CCS capacity as a part of their overall targets.

The White House is sure to follow new energy investments in the US with great enthusiasm, but policymakers should also pay close attention to the potential impact of energy shortages in the region, especially as they become increasingly common in the summer months. Middle East LNG importers may be attracted to US LNG cargoes for their comparably low costs and more flexible supply agreements than those offered by some regional producers, but any incentives that scale back US support for renewable energy development in the region are highly likely to represent missed opportunities in which the US could work to support “energy sovereignty” of its partners. The US seems likely to maintain stepped-up engagement with the Middle East in Q3. And if the White House is intent on pursuing an increasingly investment-driven approach to foreign policy, this may yield opportunities to support overall stability in key countries via measures that provide longer-term support geared toward establishing more secure access to low-cost energy supplies.

Colby Connelly is a Senior Fellow at MEI. He is also a senior analyst at Energy Intelligence, where he works with the firm’s research and advisory practices.

Top photo: Saudi Energy Minister Abdulaziz bin Salman Al Saud delivers a speech at the opening ceremony of the 9th OPEC International Seminar in Vienna, Austria, on July 9, 2025. Photo by He Canling/Xinhua via Getty images.

Three Long-Term Effects of Trump 2.0’s Middle East Approach on US Foreign Policy

What the Gulf (and America) Can Learn from Ukraine