This piece is part of the series “All About China”—a journey into the history and diverse culture of China through short articles that shed light on the lasting imprint of China’s past encounters with the Islamic world as well as an exploration of the increasingly vibrant and complex dynamics of contemporary Sino-Middle Eastern relations. Read more ...

Asia’s gas consumption has doubled in the past two decades.[1] During that time, the region has emerged as the primary driver of the growing world market for natural gas and liquefied natural gas (LNG).[2] Today, Asia is home to 59% of the world’s existing LNG import capacity and 70% of global capacity in development.[3] The International Energy Agency (IEA), which has forecast that Asian economies will account for almost half of global gas consumption to 2025, expects LNG to play a pivotal role in meeting rising gas demand in Asia.[4]

China is the world’s fastest growing gas market. Since 2017, natural gas consumption has surged in China, propelled by government efforts to move industry and households from coal to gas to combat pollution.[5]Last year, Chinese demand for natural gas grew at the fastest rate on record, with imports registering an increase of 19.9% year-on-year.[6] China imported more LNG in 2021 than any other country, accounting for nearly 60% of global LNG demand growth.[7]

This year, however, with the economy struggling, Chinese authorities have focused on securing supply and containing costs. As a result, China’s LNG imports have slowed,[8] further contributing to a global LNG market of unprecedented volatility and uncertainty. Developments in the Chinese gas market are of great significance to Qatar, which has sought to capitalize on China’s demand growth as well as its expanding overseas investment activities.

China’s LNG Appetite

China is the world’s sixth-largest natural gas producer, third-largest consumer, and second-largest importer. Although gas constitutes a modest share of China’s primary energy consumption, it nonetheless has become Beijing’s transition fuel of choice.[9] Over the past decade, China’s natural gas consumption has sharply increased, amid a government campaign to combat pollution and encourage coal-to-gas switching. [See Figure 1.]

Figure 1. Gas Consumption in China from 1998 to 2021 in billion cubic metres (bcm)

Source: BP Statistical Review of World Energy 2022; 2011; and 2007.

Historically, the industrial sector has dominated gas demand in China, though in recent years the power generation and residential sectors have also recorded rapid consumption growth. Strong pockets of industrial demand can be found in the manufacturing hubs of Jiangsu, Guangdong, and Shandong provinces. But it is important to note that consumption volumes vary greatly across regions, depending on proximity to production areas and strength of import capacity, among other factors.[10]

Domestic gas accounts for over half of China’s supply and consumption, drawn from three gas production areas, namely the Ordos Basin, the Sichuan-Chongqing Basin, and the Tarim Basin in Xinjiang. However, China’s domestic production has not kept pace with consumption growth. In 2006, China became a net importer of natural gas. Since then, pipeline gas and LNG imports have risen steadily and steeply. [See Figure 2.]

Figure 2. China’s Pipeline Gas and LNG Imports from 2011 to 2021 in billion cubic metres (bcm)

Source: BP Statistical Review of World Energy 2022

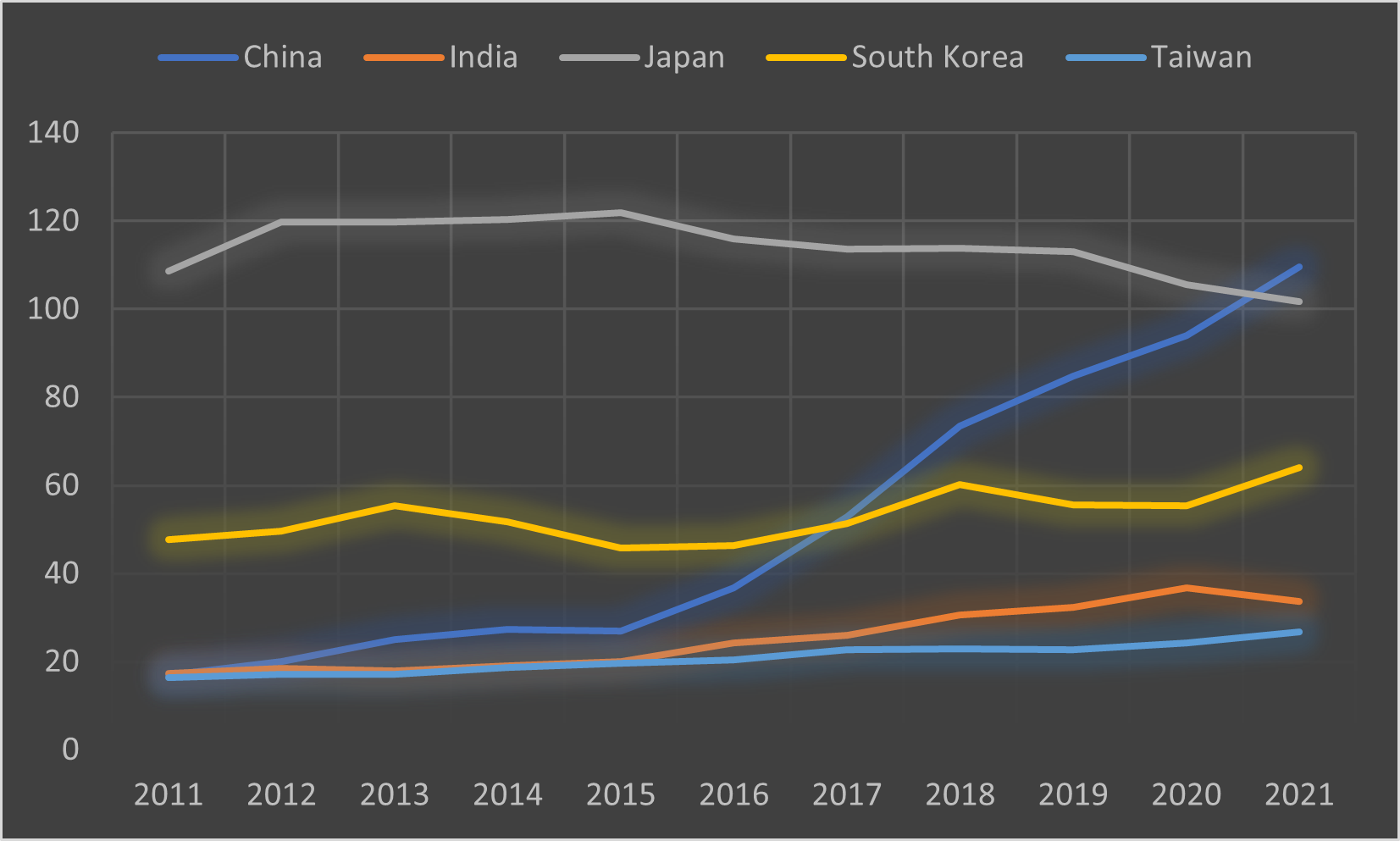

LNG is not China’s predominant source of natural gas, but rather the means to close the demand gap between domestic gas production and pipeline imports.[11] For more than a decade, the volume of Chinese LNG imports has more than doubled that of imported pipeline gas. Last year, China became the world’s top LNG buyer, surpassing Japan. [See Figure 3.] And although demand slackened in the first half of this year, according to CNPC’s Economics & Technology Research Institute (ETRI), imported LNG and pipeline gas are expected to account for 30% and 15% of the total supply in 2022, respectively.[12]

Figure 3. Annual LNG Imports of Selected Countries from 2010 to 2021 bcf/d

Source: BP Statistical Review of World Energy 2022

China imports natural gas through three pipeline systems: the Central Asia gas pipeline (from Turkmenistan, Kazakhstan, and Uzbekistan); the China-Myanmar pipeline; and the “Power of Siberia” pipeline, which delivers gas from the Russian Far East to the northern part of the country and whose southern section is in the final stages of construction. With LNG imports growing rapidly, new participants and existing domestic players are investing in China’s LNG infrastructure build-out. There are 24 receiving terminals scheduled for completion by 2025, which would nearly double the country’s import handling capacity.[13]

Although China imports a massive volume of gas, it is less dependent on foreign sources of pipeline gas and LNG, and its supply sources are more diversified than other top gas-importing countries (e.g., Japan, Germany, and Korea).[14] Even so, most of China’s import volume depends on a relatively small number of countries. [See Figures 4 and 5.]

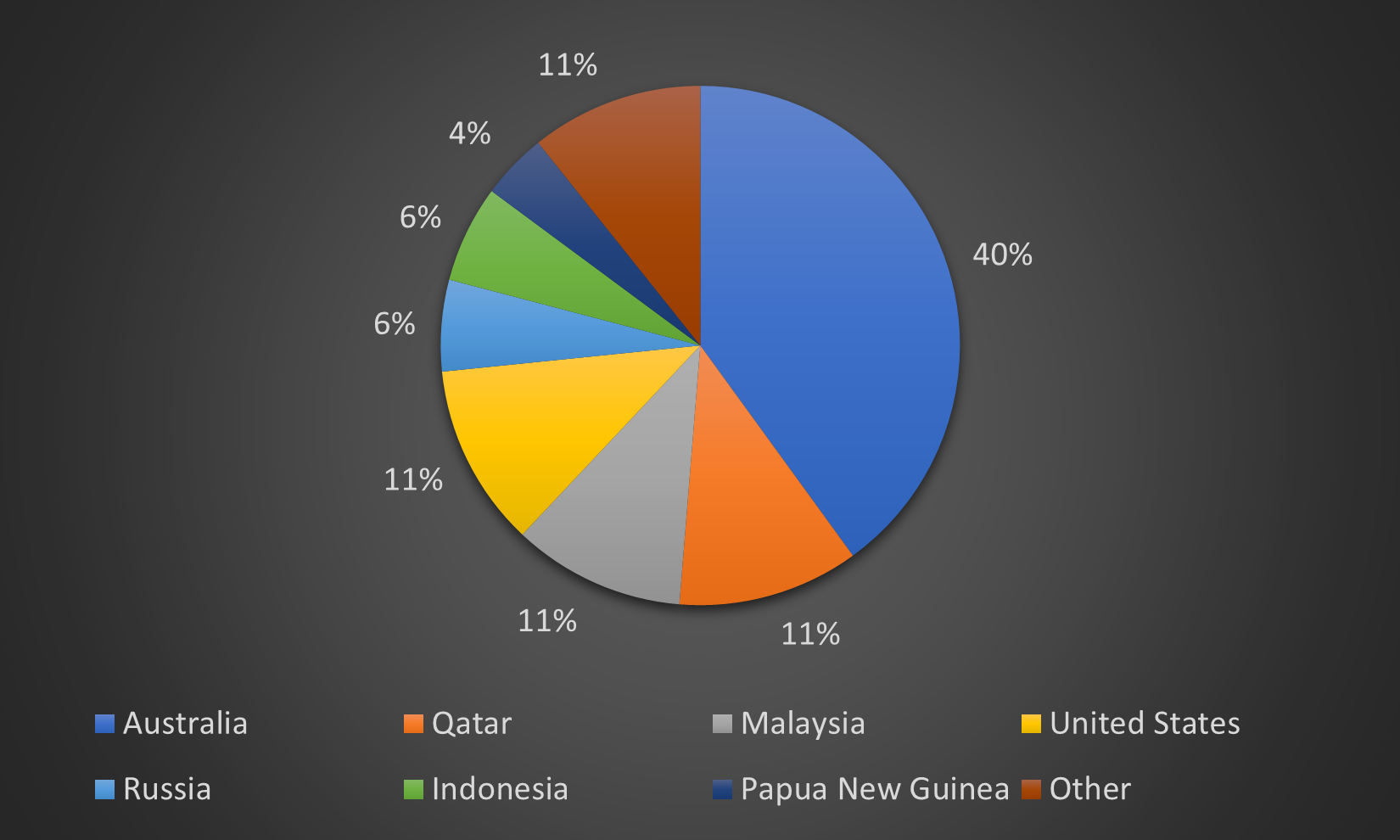

Figure 4. China’s Top Sources of LNG Imports in 2021 in billion cubic metres (bcm)

Source: BP Statistical Review of World Energy 2022

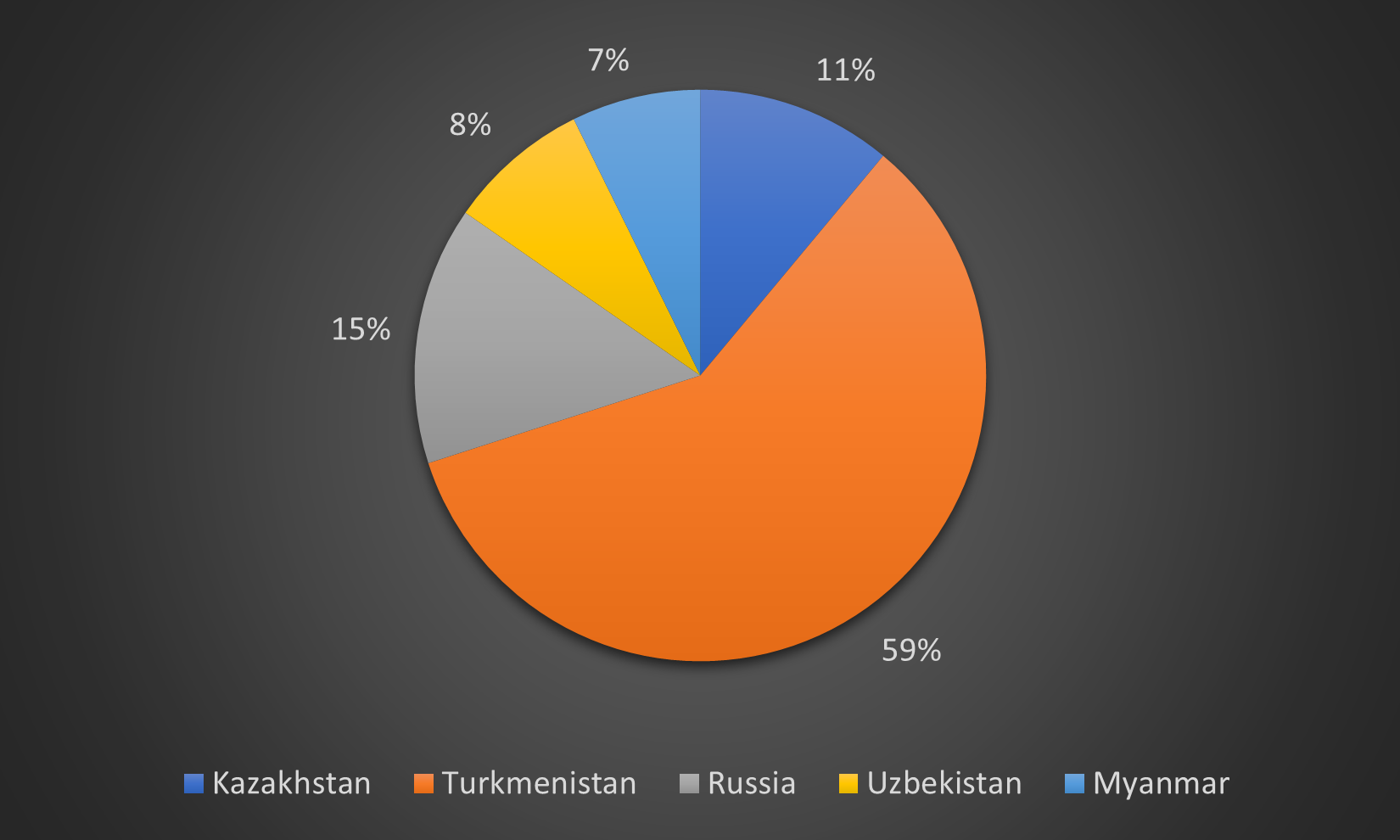

Figure 5. China’s Top Sources of Pipeline Gas Imports in 2021 in billion cubic metres (bcm) Source: BP Statistical Review of World Energy 2022

Source: BP Statistical Review of World Energy 2022

The past decade of rapid LNG consumption and import growth in China has witnessed an expanding cast of Chinese buyers. The winter 2017-2018 gas shortage in the northern part of China not only exposed the key bottlenecks in the domestic market (i.e., an underdeveloped gas transport and storage system) but catalyzed reforms aimed at spurring competition and ensuring the security of gas supply. The ensuing liberalization of the Chinese gas market has spawned a new generation of LNG buyers.[15] Second-tier companies now operate seven of China’s 22 terminals, while smaller firms have obtained third-party access to the spare capacity of their larger counterparts.[16]

Whereas China’s “Big Three” state-owned energy enterprises — PetroChina, Sinopec and CNOOC — are obliged to ensure domestic supply, this is not the case for Chinese energy companies owned by regional governments and private-sector utilities, which are increasingly dealing directly with overseas suppliers. These companies with spot cargoes and term contracts have destination flexibility, meaning that they are generally free to divert supplies to where prices are higher. The proliferation of second-tier Chinese buyers engaged in spot purchases has complicated the marketing strategy of large LNG producers, which are mainly looking to sign long-term contracts with established customers that have firm downstream demand.[17]

Spot contracts accounted for 39% of China’s LNG imports in 2021. But contracts executed by Chinese buyers lasting 10 to 20 years make up a rapidly growing portion of those with delivery dates in 2022 and beyond. Last year, a diverse set of Chinese buyers locked into a record number of 23 long-term contracts (for a total of 27 million tons of LNG) — three-quarters of the sellers from the US, Russia, and Qatar — to hedge price risk and ensure guaranteed supply.[18]

The slew of sale and purchase agreements (SPAs) struck with American producers over the past year is one of the more striking developments in Chinese importers’ efforts to procure LNG supplies on a long-term basis, especially given the otherwise contentious US-China bilateral relationship. [See Table 1.]

Table 1. Long-Term SPAs with US Producers (2021-2022) in million tonnes per annum (mt/pa)[19]

|

Date |

Chinese Importer |

US Producer |

Contract Terms |

|

October 11, 2021 |

ENN |

Cheniere Energy, Inc. |

13-year, .9 mt/pa |

|

November 4, 2021 |

Sinopec |

Venture Global |

20-year, 4 mt/pa |

|

November 4, 2021 |

UNIPEC |

Venture Global |

20-year, 3.5 mt/pa |

|

November 5, 2021 |

Sinochem |

Cheniere Energy, Inc. |

17.5-year, mt/pa |

|

November 24, 2021 |

Foran Energy Group, Ltd. |

Cheniere Energy, Inc. |

20-year, .3 mt/pa |

|

March 22, 2022 |

Guangdong Energy Group Natural Gas Co. |

NextDecade Corp. |

20-year, 1.5 mt/pa |

|

March 29, 2022 |

ENN (2 SPAs) |

Energy Transfer |

20-year, 1.8 mt/pa and .9 mt/pa |

|

July 5, 2022 |

China Gas Hongda Energy Trading |

NextDecade Corp. |

20-year, 1.5 mt/pa |

|

July 25, 2022 |

PetroChina |

Cheniere Energy, Inc. |

25-year |

It is important to note that the recent deals between Chinese importers and US LNG producers, made possible by tariff waivers issued by Beijing two years ago,[20] have been executed in a climate marked by volatile spot prices, a tightening supply outlook, and the disruptive effects of the war in Ukraine.

The post-invasion Western sanctions against Russia and the latter’s responses to them have, among other things, fueled European demand for LNG and triggered the redirection of global LNG trade flows. Since the war began, US suppliers with destination flexibility in their contracts have delivered more LNG supplies, at premium prices, to European countries seeking larger volumes to compensate for lower pipeline imports from Russia and to fill low natural gas inventories.[21] In the meantime, Chinese gas demand has weakened, due to the country’s economic slowdown, rising gas import prices, Beijing’s policy support for clean coal, and a warmer-than-usual winter.[22] The softer Chinese demand for LNG has, in turn, had the salutary effect of freeing up supplies for major European buyers scrambling to wean themselves off Russian gas. The combined effects of slackened Chinese and increased European demand for LNG resulting from the fallout from the conflict in Ukraine can also be seen in the pattern of Chinese LNG purchases during the first half of this year, with the volume of imports from the US and Australia tumbling and imports from Russia and Qatar growing.[23]

China’s Place in Qatar’s LNG Future

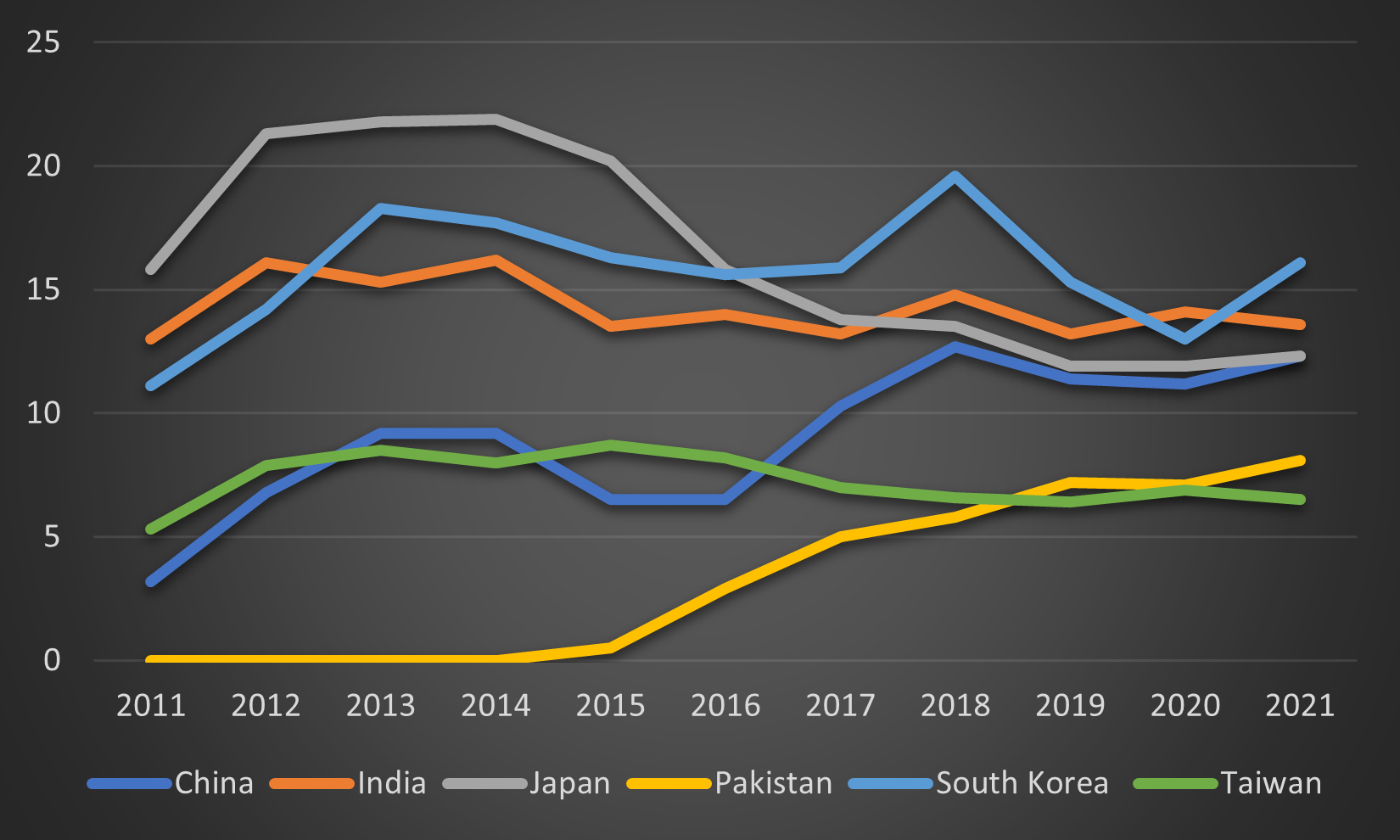

Of the five MENA countries with the largest reserves — Iran, Qatar, UAE, Saudi Arabia, and Iraq — Qatar has been the leading exporter of LNG. Historically, Qatar’s biggest market for LNG has been Asia. Over the past decade, China has become a major and increasingly important destination for Qatari LNG exports. [See Figure 6.] Home to the world’s top five LNG importing countries (China, Japan, South Korea, India, and Taiwan), Asia accounted for 72% of global LNG imports in 2021 while also accounting for 72% of Qatar’s LNG exports.

Figure 6. Qatar’s Top Asian LNG Destinations from 2011 to 2021 in billion cubic metres (bcm)

Sources: BP Statistical Review of World Energy 2022; 2021; 2020; 2019; 2018; 2017; 2016; 2015; 2014; 2013; and 2012.

Facing stiffening competition from the US and Australia, Qatar has moved to tighten its grip on the Asian, and especially the Chinese LNG market, with a series of long-term deals.[24] Last September, Qatar Petroleum (QP) signed a 15-year SPA with CNOOC Gas and Power Trading & Marketing Ltd., a subsidiary of China National Offshore Oil Corp.[25] Several weeks later, three additional long-term SPAs were struck: QatarEnergy (QE), with Guangdong Energy (10 years, starting in 2024); Qatargas, with S&T International Natural Gas Trading (15 years, starting 2023); and Qatar Liquified Gas, with China Suntien Green Energy (15 years, starting end-2022).[26]

Although long-term contracted volumes have been, and remain, the cornerstone of Qatar’s LNG strategy to maintain and build market share, the country’s gas exporters lately have shown some flexibility, signing shorter contracts and bidding competitively in spot tenders to tap into the lucrative Chinese market. Over the past year, Qatar has delivered strip tender cargoes to several second-tier Chinese companies (Beijing Gas, ENN, and Guangdong Energy) as well as to state-run China National Offshore Oil Company (CNOOC).[27]

In conjunction with its efforts to engage international partners in LNG production capacity expansion,[28] QE awarded the engineering, procurement, and construction (EPC) contract to add four new LNG export trains at North Field East to joint venture partners China’s Wison Engineering (Wison) and Spain’s Técnicas Reunidas SA (TR).[29] In addition, the state-owned China National Petroleum Corporation (CNPC) and Sinopec have reportedly entered advanced talks to invest $29 billion in the North Field East expansion project that will provide each with a 5% stake in two separate export trains and enable them to buy the fuel under long-term supply contracts.[30]

The strengthening gas trade and (pending) investment ties between the two countries have been augmented by collaborative efforts to ensure that Qatar can meet its LNG fleet requirements. Last October, as part of Qatar’s fleet expansion and replacement program, QE placed orders for four LNG carriers (to be delivered in 2024 and 2025) with Hudong-Zhonghua Shipbuilding Group Co., Ltd. (Hudong), a wholly owned subsidiary of China State Shipbuilding Corporation Limited (CSSC).[31]

Yet, some recent market reports have revised Asian demand forecasts downward, though they still expect the region to drive medium-term global demand growth.[32] LNG demand in Japan and South Korea — two key markets for Qatari exports — is widely expected to decline through 2030.[33] In the meantime, the expiry of some of Qatar’s long-term contracts with Japanese buyers could result in increased flows to China provided that the latter’s demand for LNG recovers.

Indeed, when and at which rate China’s LNG demand growth rebounds is no small matter for Qatar. After all, last year China accounted for 11% of Qatari LNG exports. In addition, China dominated term contracting in 2021, with an average length of 15 years.[34] China’s increasing reliance on term contracts in times of high spot prices[35] and the country’s expanding regasification capacity is generally good news for Qatar. But there are also downside risks. In the near term, China’s LNG demand trajectory and imports pattern will depend on the extent of the country’s economic contraction and the duration of COVID-19 restrictions partially responsible for causing it. Furthermore, high price expectations could lead China to boost domestic coal output, accelerate the development of renewables, and/or ramp up gas pipeline purchases from Russia and Turkmenistan.

Facing intensifying competition in an increasingly interconnected global LNG market, Qatar has some notable advantages: an ideal location between Europe and Asian markets; exceptionally low production costs; an established infrastructure; and a production chain with a relatively low carbon intensity. In addition, QatarEnergy’s plans to boost exports appear to be on track, with the North Field East (NFE) expansion set to produce gas in 2026 and increase LNG production to 127 million tonnes annually by 2027 from 77 million tonnes.[36] Specifically regarding the battle for market share in China, Qatar also has potential leverage: As a leading LNG producer-exporter, Qatar can assist China in diversifying long-term supply and thereby mitigate the geopolitical risks associated with overreliance on US-origin and Australia-origin cargoes.

Conclusion

Last year, China overtook Japan to become the world’s largest LNG importer. In the first six months of 2022, however, Chinese LNG purchases fell 20% y/y. This reversal, though largely attributable to economic conditions and government policies in China, is also a function of price volatility and supply disruptions in the global LNG market.

The global market is currently marked by tight demand and record high prices — a condition that shows little sign of substantial improvement in the near term. It is likely to be at least three years before new production capacity in Qatar and elsewhere brings LNG supplies back into balance with demand. Until then, demand by European nations seeking to reduce their dependency on Russian gas will likely increase. In fact, surging European demand has already sparked a bidding war for limited LNG supplies.

Qatar cannot inoculate itself against the vicissitudes of the global market. Neither can Qatar, China, or the two together prevent the erosion of confidence in the potential of natural gas to serve as an affordable “transition fuel” to renewable energy if high prices and supply disruptions persist.

[1] International Energy Agency (IEA), Evolution of global gas demand, 2005-2021, https://www.iea.org/data-and-statistics/charts/evolution-of-global-gas-demand-2005-2021; and IEA, Asia Pacific, https://www.iea.org/regions/asia-pacific#analysis.

[2] Ibid.

[3] Robert Rozansky, Asia’s Gas Lock-in, Global Energy Monitor, October 2021, https://globalenergymonitor.org/wp-content/uploads/2021/10/GEM_AsiaGas2021_FINAL.pdf.

[4] International Energy Agency (IEA), Gas Market Report, Q3-2022: 21, https://iea.blob.core.windows.net/assets/c7e74868-30fd-440c-a616-488215894356/GasMarketReport%2CQ3-2022.pdf; International Gas Union (IGU), World LNG Report 2022, https://www.igu.org/resources/world-lng-report-2022/; and Jessica Jaganathan, Scott Disavino, and Brijesh Patel, “Record oil prices slow LNG investment in Asia; North America scrambles on exports,” Reuters, October 7, 2021, https://www.reuters.com/business/energy/record-gas-prices-slow-lng-investment-asia-namerica-scrambles-exports-2021-10-07/.

[5] Akira Miyamoto and Chikako Ishiguro, “The Outlook for Natural Gas and LNG in China in the War against Air Pollution, Oxford Institute for Energy Studies, December 2018, https://ora.ox.ac.uk/objects/uuid:8f5ef73a-07f7-4326-93ca-2461f87d2249/download_file?safe_filename=The-Outlook-for-Natural-Gas-and-LNG-in-China-in-the-War-against-Air-Pollution-NG139.pdf&file_format=application%2Fpdf&type_of_work=Working+paper.

[6] Agomani Ghosh, “CHINA DATA: Total natural gas imports rose 20% in 2021 on strong energy demand,” S&P Global, January 20, 2022, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/012022-china-data-total-natural-gas-imports-rose-20-in-2021-on-strong-energy-demand.

[7] BP Statistical Review of World Energy (2022): 3, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2022-full-report.pdf.

[8] Ann Koh and Stephen Stapczinski, “China Going Quiet on LNG Hides Risk That May Upend Global Market,” Bloomberg, July 26, 2022, https://www.bnnbloomberg.ca/china-going-quiet-on-lng-hides-risk-that-may-upend-global-market-1.1797360.

[9] Wenran Jiang, “China’s LNG Market: Past, Present and Future,” Canadian Global Affairs Institute (CGAI), August 2019, https://www.cgai.ca/chinas_lng_market_past_present_and_future.

[10] Jian Li et al., “Natural gas industry in China: Development situation and prospect,” Natural Gas Industry B 7, 6 (2020): 604-613, https://reader.elsevier.com/reader/sd/pii/S2352854020301042?token=A5A334D107F65065235424059247850DF104C7422C8CCCF0D51A5B8927AD72A049B8ABA37BFED0BCD936E3B2A31055B3&originRegion=us-east-1&originCreation=20220815155905.

[11] Abel Meza and Muammer Koç, “The LNG trade between Qatar and East Asia: Potential impacts of unconventional energy resources on the LNG sector and Qatar's economic development goals,” Resources Policy 70 (2021), https://doi.org/10.1016/j.resourpol.2020.101886.

[12] Kshitiz Goliya, “China signed record high 22.7 mil mt of LNG term contracts in 2021: CNPC ETRI,” S&P Global, April 15, 2022, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/041522-china-signed-record-high-227-mil-mt-of-lng-term-contracts-in-2021-cnpc-etri.

[13] Rozansky, Asia’s Gas Lock-in, p. 7; Xu Yihe, “China now world top LNG importer,” Petroleum Economist, March 17, 2022; “China dominates LNG regasification capacity additions in Asia by 2025,” Offshore Technology, November 2, 2021, https://www.offshore-technology.com/comment/china-lng-regasification-2025/.

[14] Batt Odgerel, “Fueling the Dragon: Understanding China’s Natural Gas and LNG Demand,” Energy Policy Research Foundation, Inc. (EPRINC), May 2022, https://eprinc.org/wp-content/uploads/2022/05/Odgerel-Fueling-the-Dragon-May-2022_final.pdf.

[15] Sylvie Cornot-Gandolphe, “China’s Quest for Blue Skies: The Astonishing Transformation of the Domestic Gas Market,” Etudes de l'Ifri, September 2019, https://www.ifri.org/sites/default/files/atoms/files/cornot-gandolphe_china_domestic_gas_market_2019.pdf.

[16] Batt Odgerel, “Fueling the Dragon;” and Cindy Liang and Abache Abreu, “ANALYSIS: China's latest energy liberalization policy set to break oil and gas monopolies,” S&P Global, June 6, 2019, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/natural-gas/060619-analysis-chinas-latest-energy-liberalization-policy-set-to-break-oil-and-gas-monopolies#:~:text=%22The%20move%20aims%20to%20break,terminals%20and%20underground%20gas%20storage.

[17] Cindy Liang and Eric Yap, “Analysis: China's new crop of LNG buyers complicates Qatar’s long-term sales strategy,” S&P Global, June 18, 2021, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/natural-gas/061821-analysis-chinas-new-crop-of-lng-buyers-complicates-qatars-long-term-sales-strategy.

[18] Hirofumi Matsuo, “China locks in record long-term LNG deals to bolster energy security,” Nikkei Asia, July 11, 2022.

[19] “Cheniere and ENN Sign Long-Term LNG Sale and Purchase Agreement,” Cheniere Press Release, October 11, 2021, https://lngir.cheniere.com/news-events/press-releases/detail/231/cheniere-and-enn-sign-long-term-lng-sale-and-purchase; “Venture Global and Sinopec Announce Historic LNG Sales and Purchase Agreements,” Venture Global Press Release, November 4, 2021, https://venturegloballng.com/press/venture-global-and-sinopec-announce-historic-lng-sales-and-purchase-agreements/; “Cheniere and Sinochem Group Sign Long-Term LNG Sale and Purchase Agreement,” Cheniere Press Release, November 5, 2021, https://lngir.cheniere.com/news-events/press-releases/detail/234/cheniere-and-sinochem-group-sign-long-term-lng-sale-and; “Cheniere and Foran Energy Group Sign Long-Term LNG Sale and Purchase Agreement,” Cheniere Press Release, November 24, 2021, https://lngir.cheniere.com/news-events/press-releases/detail/235/cheniere-and-foran-energy-group-sign-long-term-lng-sale-and; NextDecade, “NextDecade and Guangdong Energy Announce Binding Heads of Agreement,” Press Release, March 24, 2022, https://investors.next-decade.com/news-releases/news-release-details/nextdecade-and-guangdong-energy-announce-binding-heads-agreement; NextDecade, “NextDecade and ENN Execute 1.5 MTPA LNG Sale and Purchase Agreement,” Press Release, April 6, 2022, https://investors.next-decade.com/news-releases/news-release-details/nextdecade-and-enn-execute-15-mtpa-lng-sale-and-purchase; NextDecade, “NextDecade and Guangdong Energy Announce Binding Heads of Agreement,” Press Release, March 24, 2022, https://investors.next-decade.com/news-releases/news-release-details/nextdecade-and-guangdong-energy-announce-binding-heads-agreement; and “PetroChina signs long-term SPA with Cheniere for 2.5 bcm/year of LNG (US),” Enerdata, July 22, 2022, https://www.enerdata.net/publications/daily-energy-news/petrochina-signs-long-term-spa-cheniere-25-bcmyear-lng-us.html.

[20] Nikos Tsafos, “A New Chapter in U.S.-China LNG Relations,” CSIS, December 6, 2021, https://www.csis.org/analysis/new-chapter-us-china-lng-relations; Brian Spegele, “China Binges on U.S. Gas to Manage Energy Shortage, Carbon Footprint,” Wall Street Journal, November 2, 2021, https://www.wsj.com/articles/china-binges-on-u-s-gas-to-manage-energy-shortage-carbon-footprint-11635845401?mod=article_inline; and Jiaxin Jiang, “China’s LNG imports Outlook: Can the United States Capture More of the Market?” RBAC Inc., April 13, 2021, https://rbac.com/chinas-lng-imports-outlook-can-the-united-states-capture-more/.

[21] US Energy Information Agency (EIA), “The United States became the world’s largest LNG exporter in the first half of 2022,” Today in Energy, July 25, 2022, https://www.eia.gov/todayinenergy/detail.php?id=53159.

[22] “China’s LNG imports to see unprecedented decline in 2022,” Wood Mackenzie, July 19, 2022, https://www.woodmac.com/press-releases/chinas-lng-imports-to-see-unprecedented-decline-in-2022/#:~:text=China's%20LNG%20imports%20are%20set,to%20slow%20down%20in%202022; and Chen Aizhu, “China’s LNG imports set for first big decline as demand wanes,” Reuters, May 27, 2022, https://www.reuters.com/business/energy/chinas-lng-imports-set-first-big-decline-demand-wanes-2022-05-27/.

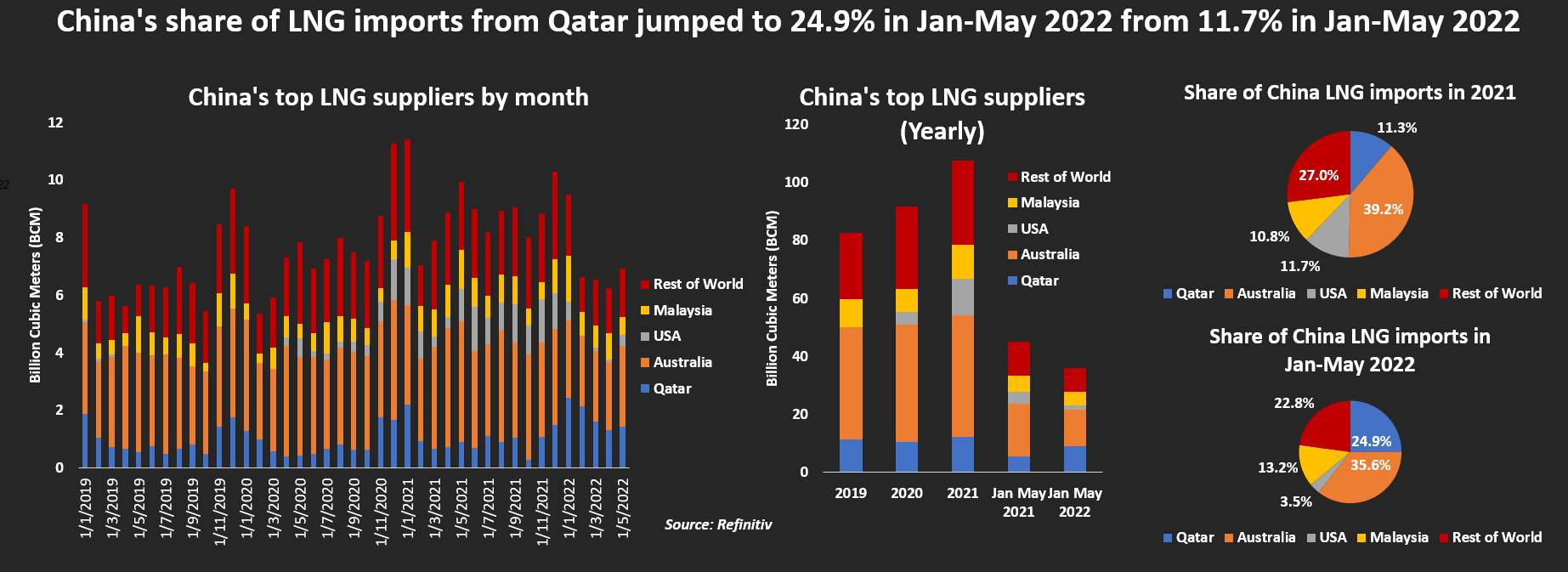

[23] During January-May 2022, China’s share of LNG imports from Qatar rose to 24.9%, from 11.7% in 2021, Reuters, https://fingfx.thomsonreuters.com/gfx/ce/mypmnrgnbvr/ChinaLNGfromQatar.png.

{kind=link}

[24] “Qatar Seeks to Maintain Momentum in Asian LNG Markets,” LNG Journal.com, July 21, 2022, https://lngjournal.com/index.php/market-tracker/item/103486-qatar-seeks-to-maintain-momentum-in-asian-lng-markets.

[25] Claudia Carpenter and Adithya Ram, “Qatar signs 15-year deal to sell China 3.5 mil mt/yr LNG,” S&P Global, September 29, 2021, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/092921-qatar-signs-15-year-deal-to-sell-china-35-mil-mtyr-lng.

[26] “Sinopec gets 1st Qatar LNG cargo from new agreement,” Offshore Energy, January 18, 2022, https://www.offshore-energy.biz/sinopec-gets-1st-qatar-lng-cargo-from-new-agreement/.

[27] “Qatar courts China for funding and LNG offtake from North Field expansion,” LNG Journal.com, September 6, 2021, https://lngjournal.com/index.php/china/item/103810-qatar-courts-china-for-funding-and-lng-offtake-from-north-field-expansion.

[28] Wayne Ackerman, “Qatar strengthens ties with international energy players through North Field East Project,” Middle East Institute, July 5, 2022, https://www.mei.edu/publications/qatar-strengthens-ties-international-energy-players-through-north-field-east-project.

[29] Pat Davis Szymczak, “Spanish-Chinese JV Wins EPC Contract for Qatar’s North Field LNG Expansion,” Journal of Petroleum Technology, May 12, 2022, https://jpt.spe.org/spanish-chinese-jv-wins-epc-contract-for-qatars-north-field-lng-expansion.

[30] Chen Aizhu, “EXCLUSIVE-China firms in advanced talks with Qatar for gas field stakes, LNG offtake – sources,” Reuters, June 17, 2022, https://www.reuters.com/article/china-qatar-lng-idAFL4N2Y31YX; and “China in Talks With Qatar for Gas Stakes Worth Billions,” Bloomberg, June 17, 2022, https://www.bloomberg.com/news/articles/2022-06-17/china-in-talks-with-qatar-for-gas-field-stakes-reuters-says?srnd=markets-vp#xj4y7vzkg.

[31] Katherine Si, “Qatar Petroleum building four LNG carriers at Hudong Zhonghua,” Seatrade Maritime News, October 11, 2021, https://www.seatrade-maritime.com/shipyards/qatar-petroleum-building-four-lng-carriers-hudong-zhonghua. See also: “Qatar Petroleum enters agreement that could reach QR 11 B to reserve LNG shipyard capacity in China,” Gas Processing News, May 4, 2021, http://gasprocessingnews.com/news/qatar-petroleum-enters-agreement-that-could-reach-qr-11-b-to-reserve-lng-shipyard-capacity-in-china.aspx.

[32] See, for example, IEA, Gas Market Report, Q3-2022 (July 2022): 32, https://iea.blob.core.windows.net/assets/c7e74868-30fd-440c-a616-488215894356/GasMarketReport%2CQ3-2022.pdf; and “Global LNG Market Outlook 2022-26,” Bloomberg New Energy Finance, June 16, 2022, https://bbgmktg.turtl.co/story/global-lng-market-outlook/page/1?bbgsum-page=DG-WS-PROF-BLOG-POST-139527&tactic-page=602005.

[33] Sam Reynolds, “The Economic Case for LNG in Asia is Crumbling,” Institute for Energy Economics and Financial Analysis (August 2022): 24-29, https://ieefa.org/media/2949/download?attachment.

[34] Shell LNG Outlook 2022 (February 2022): 26, https://www.shell.com/promos/energy-and-innovation/v1/lng-outlook-2022-report/_jcr_content.stream/1645378179742/3399fc5b65329ddf5fda80ad6cf2f6eab2abd9e5/shell-lng-outlook-2022.pdf.

[35] Independent Commodity Intelligence Services (ICIS), ICIS LNG Global Supply & Demand Outlook – 2022 (February 2022): 9, https://cjp-rbi-icis.s3.eu-west-1.amazonaws.com/wp-content/uploads/sites/7/2022/02/11183252/ICIS-2022-Global-LNG-Supply-and-Demand-Forecast.pdf.

[36] Maha El Dahan and Andrew Mills, “EXCLUSIVE Qatar has not approached Asian buyers over gas diversions to Europe,” Reuters, February 3, 2022, https://www.reuters.com/markets/europe/exclusive-qatar-has-not-approached-asian-buyers-over-gas-diversions-europe-2022-02-03/.

The Middle East Institute (MEI) is an independent, non-partisan, non-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.