The Russia-Ukraine War has Turned Egypt's Food Crisis into an Existential Threat to the Economy

March 3, 2022

Share

With the outbreak of the Russia-Ukraine war on Feb. 24, 2022, Egypt’s food security crisis now poses an existential threat to its economy. The fragile state of Egypt’s food security stems from the agricultural sector’s inability to produce enough cereal grains, especially wheat, and oilseeds to meet even half of the country’s domestic demand. Cairo relies on large volumes of heavily subsidized imports to ensure sufficient as well as affordable supplies of bread and vegetable oil for its 105 million citizens. Securing those supplies has led Egypt to become the world’s largest importer of wheat and among the world’s top 10 importers of sunflower oil. In 2021, Cairo was already facing down food inflation levels not seen since the Arab Spring civil unrest a decade earlier that toppled the government of former President Hosni Mubarak. After eight years of working assiduously to put Egypt’s economic house back in order, the government of President Abdel-Fattah el-Sisi is now similarly vulnerable to skyrocketing food costs that are reaching budget-breaking levels.

The Russia-Ukraine war catapulted prices to unsustainable levels for Egypt, increasing the price of wheat by an additional 44% and that of sunflower oil by 32% virtually overnight. Even more troublesome, the war also threatens Egypt’s physical supply itself since 85% of its wheat comes from Russia and Ukraine, as does 73% of its sunflower oil. With activity at Ukraine’s ports at a complete standstill, Egypt already needs to find alternative suppliers. A further escalation that stops all Black Sea exports could also take Russian supplies off the market with catastrophic effect. With about four months of wheat reserves, Egypt can meet the challenge, but to do so, Cairo will need to take immediate and decisive action, which can be made even more effective with the timely support of its American and European partners.

Bread, Protests, and Subsidies

Egypt’s massive wheat imports are driven by the widespread consumption of the traditional round flatbread known as eish baladi, a popular staple of every meal among the country’s working poor. Egyptians consume 150-180 kilograms of bread per capita, more than double the global average of 70-80 kg. Keeping the price of Egypt’s staple food affordable has been the bedrock of regime stability since the Free Officers revolution brought then-President Gamal Abdel Nasser to power 60 years ago. When Nasser’s successor acceded to World Bank and International Monetary Fund (IMF)-mandated subsidy cuts on wheat flour, cooking oil, and other staples, it triggered Egypt’s infamous 1977 “bread riots.” The gravity of the crisis compelled then-President Anwar Sadat to call out the army to suppress the protesters. Sadat’s successor, Mubarak, fared far worse when Egypt’s annual food inflation reached 18.9% in 2011 amid another round of World Bank and IMF-mandated subsidy cuts. Soaring bread prices — due in part at the time to a weather-related, lower-than-expected Russian wheat crop — kept Egypt’s working class on the streets, sustaining the protest movement for justice and dignity that toppled Mubarak and ended his 30-year rule.

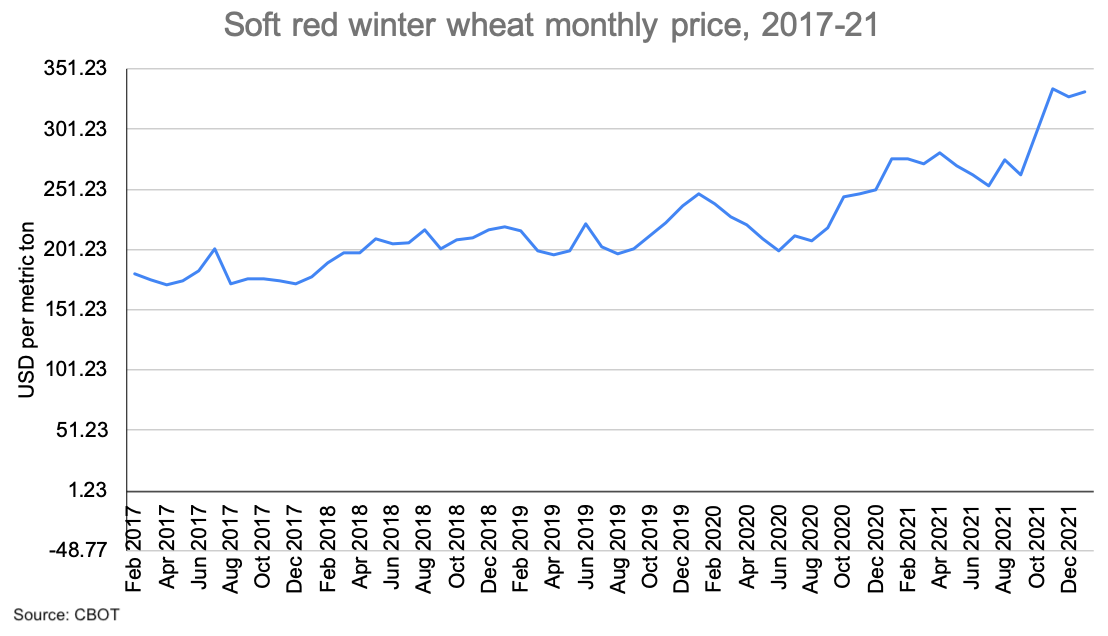

Now Egypt again faces a severe wheat shortfall amid soaring prices. According to estimates from the United States Department of Agriculture (USDA), Egypt’s wheat production in marketing year (MY) 2021/22 will reach 9.0 million metric tons (MMT) while its consumption will total 21.3 MMT, leaving a 12.3 MMT shortfall to be made up with imports. Even prior to Russia’s invasion of Ukraine, the prices for those imports were at record levels. As detailed in a previous Middle East Institute publication, the global average price for cereal grains increased 27.3% in September 2021 compared to September of the previous year and since then it has continued to climb at an even faster rate. The price of soft wheat used in bread manufacture stood at $271 per ton at the end of the third quarter of 2021, a 22% year-on-year increase. The price in the fourth quarter of 2021 shot up further as global inventories fell after producers in the U.S., Canada, Russia, Ukraine, and the rest of the Black Sea region experienced crop damage due to droughts, frost, and heavy rain. As of March 3, 2022, just seven days into Russia’s Ukraine invasion, the end of day settlement price for the March 2022 soft wheat contract on the Chicago Board of Trade stood at nearly $389 per ton.

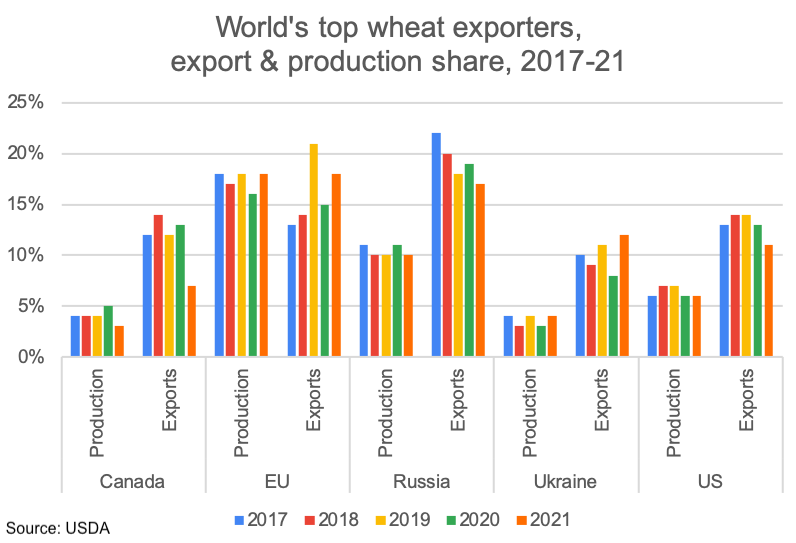

With Russia being the world’s largest wheat exporter and Ukraine the fifth largest, accounting for a combined total of 30% of global wheat exports, prices are likely to remain elevated for the duration of the war. And the cost for Egypt goes beyond just the import price. Egypt allocates five loaves of subsidized bread per day to each recipient participating in its rationing system. The subsidized selling price of eish baladi is EGP 0.05 per loaf (approximately 0.3 U.S. cents at the March 1, 2022 exchange rate), representing less than one-tenth the actual cost. The government’s compensation to Egypt’s bakeries costs it EGP 0.60 (3.8 cents) per eish baladi loaf. With more than 88% of Egypt’s population registered for the bread rationing system, Cairo allocated $3.3 billion for bread subsidies in its 2021/22 budget, a 10% increase over the previous year. Egypt’s new wheat purchases and subsidies will now become an even greater fiscal burden for the treasury to bear.

Egypt’s Other Oil Crisis

In addition to bread, the Russia-Ukraine war has begun to disrupt Egypt’s supply of sunflower seed oil, the country’s main vegetable oil along with soybean oil. The government imports 95% of its vegetable oil and offers Egyptian consumers a highly subsidized blend of sunflower oil and soybean oil. The USDA forecasts Egypt’s MY 2021/22 sunflower oil consumption to reach 355,000 metric tons (MT), with 350,000 MT or 98.6% being supplied by imports. Ukraine and Russia are the world’s leading exporters, collectively accounting for over three-fourths of the global export supply of sunflower oil. In 2020, Egypt imported 54.4% of its sunflower oil supply from Ukraine and 18.83% from Russia. On Feb. 28, Ukrainian sunflower oil was assessed at $1,950.50 per MT, up $470.50 from the prewar price of $1,480 per MT on Feb. 23. That price was for those who were actually able to acquire a consignment for physical delivery. The commodities price reporting firm Platts has paused Black Sea sunflower oil assessments since Feb. 24.

With Ukraine and Russia being the dominant exporters, Egypt cannot easily find replacement suppliers. It also cannot easily increase the volume of soybean oil either, as producers Argentina, Brazil, and Paraguay will experience a 9.5 million ton soybean production shortfall due to insufficient rainfall in South America’s growing regions. The global market for vegetable oils had already witnessed a perfect storm of rising prices across oils during 2021. As of June 1, 2021, Egypt raised the price of subsidized unblended vegetable oils by 23.5% while the standard issue one-liter bottle of blended soybean and sunflower oil was replaced by an 800-ml bottle at the same price, equivalent to a 20% reduction.

While the subsidy reduction was helpful in combatting the 2021 wave of global food oil inflation, the early 2022 Russia-Ukraine war has turned that wave into a price spike tsunami as countries scramble to find alternatives to sunflower oil. In January 2022, Indonesia, which produces 58% of the global supply of palm oil, placed strong limits on exports to bring down its own surging domestic cooking oil prices due to the increases in 2021. Malaysia, the next largest palm oil producer with 26% of global output, experienced lower palm oil production and will not be able to cope with heightened demand from nations seeking to find a substitute for sunflower oil, leaving Egypt still facing a vegetable oil crisis.

Global Food Supply Crunch – The China Syndrome

The global supply crunch for cereal grains, oilseeds, and vegetable oils has been hugely exacerbated by China’s hoarding of over half the world’s grain stores, including 51% of global wheat reserves. The country’s rapid industrialization and urbanization has reduced the amount of arable and contaminated key water supplies, making China’s food security vulnerable to climate change-driven extreme weather events. Heavy autumn 2021 floods have put its summer grain crops at risk, including about one-third of China’s wheat production. Beijing’s predicament was heightened by its urgent need for wheat imports to serve as livestock feed to rapidly replenish its local pig population and thereby ensure its supply of animal protein, following an African swine fever epidemic that wiped out half the nation’s pigs. China similarly controls about 38% of the world’s global soybean stores. Surging soybean prices have also hampered Chinese pig farmers’ ability to feed their herds. Two days prior to Russia’s invasion of Ukraine, China’s National Food and Strategic Reserves Administration announced that it would release soybeans and some edible oil from state reserves. Likewise, with the Chinese Communist Party’s Central Committee and China’s State Council (the country’s executive branch cabinet) concerned about the “large-scale re-emergence of poverty,” Beijing imported a record 164.5 MMT of grains in 2021, representing an 18.1% increase compared to 2020 — helping to drive the spike in global grain prices prior to Russia’s invasion of Ukraine. While Egypt and other Middle East and North Africa (MENA) region countries could suffer from supply disruptions due to a halt in Black Sea traffic, China can continue to receive Russian grain exports overland via the rail links between the two countries.

A wheat field situated near the village of Yubileiny, 2.5 km west of Lugansk, Ukraine, on July 13, 2021. Photo by Alexander RekaTASS via Getty Images.

A Helicopter Rescue for Ramadan?

So how bad off is Egypt? While the threat to Egypt’s economy is of a severe nature, the country is on a much firmer financial footing than it was in 2011 before Mubarak’s ouster. The 2015 discovery of Egypt’s Zohr offshore natural gas field, the largest in the eastern Mediterranean, combined with the 2016 macroeconomic reforms, conducted in cooperation with the IMF, turned the Egyptian economy around. By 2018 the country’s foreign reserves reached almost $40 billion, equivalent to six months of imports of goods and services. By 2019, Egypt was a net energy exporter. With the additional June 2020 staff-level agreement between Egypt and the IMF on a $5.2 billion stand-by arrangement to offset COVID-19’s adverse economic impact, Egypt experienced GDP growth of 3.6% in 2020 in contrast to the economic contractions that swept almost all the countries in the MENA region. In the first half of the fiscal year 2021-22, Egypt’s economy grew by 9% and growth is expected to exceed 6% for the whole fiscal year ending on June 30, 2022.

With greater economic resources at its disposal, the government’s General Authority for Supply Commodities (GASC) has engaged in pro-active efforts to mitigate Egypt’s food import conundrum even prior to the outbreak of the Russia-Ukraine war. Taking advantage of a late November 2021 dip in the price of wheat due to market concerns about the then-new Omicron COVID-19 variant causing a demand drop, GASC purchased 600,000 MT of Russian, Ukrainian, and Romanian wheat, obtaining heavy discounts from traders. At the outbreak the Russia-Ukraine war, Egypt had strategic wheat reserves sufficient for 4.2 months. In March 2021, Egypt’s strategic supplies of vegetable oils were sufficient to last five months.

In August 2021, President Sisi acknowledged the pressing need to move forward with bread subsidy reform and the delicate political nature of the task. Ministerial-level attention to the topic intensified during January and early February 2022 ahead of the annual March budget planning period before being upended by further price and supply shocks following Russia’s invasion of Ukraine. However, with Ramadan beginning in Egypt on April 2, 2022, entailing a month of festive family Iftar meals to break the daily fasts, policymakers in Cairo need to find quick-fix solutions to ensure affordable wheat and cooking oil supplies. In the longer term, it would be most efficient for Cairo to replace all or part of its bread subsidy with direct, cash transfer payments — what economists have nicknamed “helicopter money” — to Egypt’s working poor and other less fortunate segments of society. Yet with inflation rising, the government is unlikely to increase inflationary pressures by enlarging the country’s money supply. The more likely short-term solution, and the one favored by Egypt’s minister of supply, is to issue vouchers for bread similar to what Egyptians already receive for other subsidized food items.

Conclusion

While a severe and immediate threat, Egypt can ease the short-term price supply shocks to wheat and vegetable oil through shrewd fiscal policy and assertive acquisition efforts in cooperation with its Western partners that are also major suppliers of these commodities. Washington, Ottawa, Paris, Berlin, and Brussels should seize the initiative to assist Cairo before unrest manifests. Egypt should continue its constructive financing cooperation with the IMF as well as its Arab Gulf state partners. Ultimately, part of Egypt’s long-term solution is to increase its agricultural output by expanding its arable land and further modernizing its farming sector through advanced agri-tech, water management, and green energy technologies. The United States, Europe, and Israel are all industry leaders in these fields. Establishing joint venture investment partnerships with Egypt to increase local food production could strengthen the fragile state of Egypt’s food security and promote regional agricultural cooperation in the eastern Mediterranean and Middle East.

Professor Michaël Tanchum is a non-resident fellow with the Middle East Institute’s Economics and Energy Program. He teaches at Universidad de Navarra and is an associate senior policy fellow in the Africa program at the European Council on Foreign Relations (ECFR). He is also a senior fellow at the Austrian Institute for European and Security Policy (AIES). The author would like to thank Rafaella Vargas Reyes for her research assistance. The views expressed in this piece are his own.

Photo by Shawn Baldwin/Bloomberg via Getty Images.

The Middle East Institute (MEI) is an independent, non-partisan, not-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.