The Asia-Pacific in the "Golden Age of Gas": Implications for Middle East LNG Exporters

April 8, 2013

Share

Asian Natural Gas at the Crossroads

The recent unconventional natural gas boom and the consequent gas glut in North America has the potential to fundamentally transform the dynamics of the global natural gas industry. While natural gas prices at Henry Hub have hovered around the US$3.00–3.50/MMBtu level in recent years, prices for contracted LNG imports into Japan have commonly exceeded $14/MMBtu during the same period, spurred by rapidly growing natural gas demand in Asia. Growth in LNG flows from North America to Asia has thus become a real option for the industry.

Status of Asia-Pacific Energy Use and Trans-Pacific LNG Trade

Natural gas typically accounts for 10–20% of the energy mix in the Asia-Pacific economies, with China the major exception: only 4% of its energy needs are met by natural gas. The significance of natural gas trade to the Asia-Pacific economies is underscored by the fact that imports accounted for 37% of total natural gas use in the region in 2010.[1]

In contrast to oil, the global natural gas market is regionally segmented to a much larger degree, with intra-regional flows (i.e. the gas flows from Canada to the US or those from Southeast Asia and Australia to the Far East) and inter-regional flows (i.e. from Russia and the Central Asian economies to Europe and from the Middle East to East Asia) both significant. The Asia-Pacific economies source their natural gas imports primarily from the Middle East and from Southeast Asia (Indonesia, Malaysia, Brunei, and Australia), though Russia and the Central Asian economies are increasingly emerging as major natural gas exporters into the region. Note that North America effectively remain a “gas island” isolated from the rest of the world, with few significant trans-Pacific or trans-Atlantic gas flows. In particular, trans-Pacific LNG trade (between North America and the Asia-Pacific) only accounted for 0.3% of global natural gas trade in 2010.

Factors Driving Trans-Pacific LNG Trade

Both demand and supply factors have contributed to a scenario where significant growth in LNG exports from North America to the Asia-Pacific has become a real possibility. On the demand side, natural gas demand in the Asia Pacific is expected to grow substantially in the next 25 years. According to the International Energy Agency, Asia’s demand for natural gas is projected to increase from 400 bcm in 2010 to 1,200 bcm in 2035, an annual average compound growth rate of 4.5%.[2] World gas demand will increase by 1.8% over the same time period. Asian demand will constitute 23.5% of global gas demand by 2035, compared to its 12% share in 2010.

Two other factors could further boost the Asia-Pacific region’s future demand for LNG imports. First, Indonesia and Malaysia, two of the largest gas exporters in the region, are both experiencing dwindling supply from aging fields. Coupled with increasing domestic natural gas demand, both countries appear set to begin importing LNG even as they continue to export contracted LNG to countries such as Japan and South Korea.[3] Indonesia and Malaysia have both completed constructing their first LNG terminals this year and are expected to begin importing LNG later in the year.[4]

Second is the impact of the March 2011 earthquake and the Fukushima nuclear disaster on Japan’s LNG demand. This not only prompted the shutdown of all 50 of Japan’s nuclear reactors, but also damaged oil and coal-fired thermal power stations.[5] As Japan seeks to replace its lost thermal and nuclear capacity by running all its gas-fired units, Japan’s LNG demand has increased and may be expected to continue to do so in the short-run. Whether Japan’s LNG demand will grow even further beyond the medium term is less clear and depends on the extent to which the nuclear shutdown in Japan persists.

Asia’s growing demand for natural gas does not by itself provide a compelling reason for trans-Pacific LNG trade. The growing demand is also set to be accompanied by a large increase in North American gas production, driven by the remarkable shale gas “revolution,” which has made feasible the extraction of vast reserves of unconventional gas in the US and Canada. As such, while North America accounted for around 11% of the world’s technically recoverable conventional gas resources at the end of 2011, the figure jumps to over 16% once unconventional gas resources are included as well.

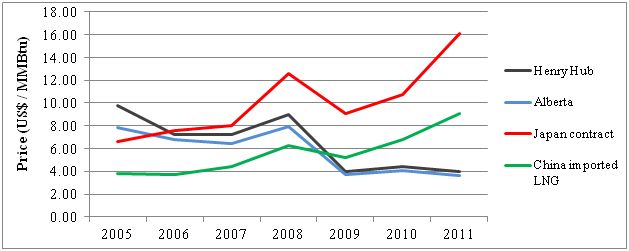

The combined effect of the North American gas glut and the Asian demand surge has been to widen natural gas price differentials between North America and Asia. Historically, natural gas in the Asia-Pacific region has been priced at a premium relative to North American natural gas. As Figure 1 illustrates, however, in the last few years the price differentials have widened considerably. While Asian prices (except for a brief decline during the 2008 recession) were generally on an uptrend, spurred by rising gas demand, North American spot prices have decreased over time to $2.50-3.50/mmbtu levels, a result of the gas glut in the continent. The differential between Henry Hub prices and Japanese contract prices in 2012 is estimated to exceed $12/MMBtu and provides the basic incentive for North American producers to export LNG to the Asia Pacific.

Figure 1: Natural Gas Prices in North America and Asia

Sources: Gas Market Outlook: May 2011 (London: Nexant, May 2011); World Gas Intelligence, Various Issues, 2010–12; Petroleum Association of Japan: Oil Statistics, 2011; Alberta Energy, 2011.

Notes: The Henry Hub and Japan spot prices for 2011 are the averages of the prices for all 12 months of 2011. The average price for China’s imported LNG in 2011 was reported in World Gas Intelligence (8 Feb 2012, 6). The Japan contract price for each month of 2011 is estimated using the assumed formula: Contract price = 0.1485*Average JCC crude price (for the 3 preceding months lagged by 1 month) + 1.0. The slope and intercept are derived from Eng (2008),[6] and is consistent with recent estimates of the oil slope amounting to 0.14-0.1485. [7] The average Japanese contract price for 2011 is then estimated by averaging the estimated monthly contract prices for 2011.

Trans-Pacific LNG Trade Initiatives

A number of LNG export projects have been proposed in both the US and Canada. All of the projects proposed in Canada are new liquefaction terminals to be located on the West Coast in British Columbia, with access to the vast reserves of mostly unconventional gas in the Western Canadian Sedimentary Basin (WCSB) that span over the provinces of Alberta and British Columbia. In contrast, the US export projects largely involve redeveloping existing import (regasification) terminals on the Gulf and East Coast into export liquefaction terminals.

In theory, the liquefaction capacity in North America could exceed 20 Bcf/d if all of the proposed export projects go through; by way of comparison, the liquefaction capacity of Qatar (currently the largest LNG exporter in the world) is 10.7 Bcf/d.[8] However, most projects are still awaiting regulatory approval and many will not see the light of day through the normal course of attrition. In the US, only the Sabine Pass LNG terminal has received full approval to export LNG, while Lake Charles, Cameron LNG, Freeport LNG, Cove Point LNG and Jordan Cove LNG have received approval to export LNG to countries having free trade agreements with the US. In Canada, Kitimat LNG and BC LNG have been authorized to export LNG while LNG Canada is still awaiting regulatory approval.

There has been growing interest in purchasing North American LNG among Asian buyers, a number of whom have already signed contracts to purchase LNG from the US. GAIL (from India) and KOGAS (from South Korea) will each purchase 3.5 mtpa (millions of tons per annum) of LNG from Cheniere’s Sabine Pass terminal under 20-year contracts. Mitsubishi and Mitsui (from Japan) will import 4 mtpa of LNG each from Cameron LNG, while Tokyo Gas and Sumitomo Corp (from Japan) have reached an initial agreement to purchase 2.3 mtpa of LNG from Cove Point LNG. In addition, GAIL, Nusantara Regas and PLN (both from Indonesia), and Osaka Gas (from Japan) are in talks with various US suppliers to import LNG.

Outlook for Trans-Pacific LNG Trade

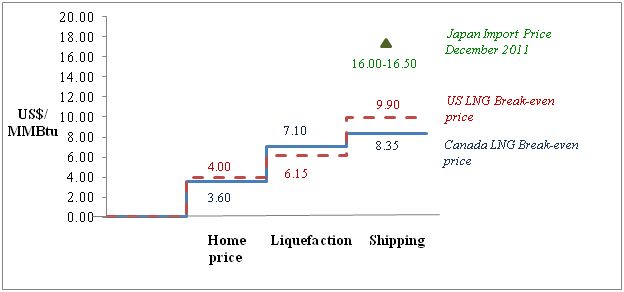

While there exist large price differentials between natural gas prices in North America and Asia, an assessment of whether exports from the USA or Canada to the Asia-Pacific are economically viable needs to take into account the additional liquefaction and shipping costs incurred in exporting gas compared to selling the gas domestically. The step-chart in Figure 2 illustrates the estimated prices at which LNG exported by US and Canada break even, and compares it to the actual price that LNG exporters can hope to obtain if they sell LNG to Japan under long-term contracts. The break-even export price is approximately $9.90/MMBtu for US Gulf Coast terminals and $8.35/MMBtu for Canadian export terminals, both of which are considerably less than the estimated Japanese contract price of $16.00-$16.50/MMBtu. Thus, at current prices it makes economic sense for gas producers in North America to export LNG to the Asia Pacific region as opposed to selling the gas domestically.

Figure 2: Illustrative Cost Build-Up for North American LNG Exports (2011)

Sources: Gas Market Outlook: May 2011 (London: Nexant, May 2011); Energy Alberta, 2011; Pehlivanova, “North American LNG Exports Complicated by Alternative Markets, Investment Costs,” Oil & Gas Journal, (October 3, 2011); World Gas Intelligence, Various Issues, 2011-2012; Petroleum Association of Japan: Oil Statistics (2011).

Notes: The home price for Canada refers to the Alberta average spot price for 2011 (Energy Alberta, 2011). The costs of liquefaction and shipping are estimated by Pehlivanova, 2011.

For US LNG exports from the Gulf Coast to remain economically feasible, a minimum price differential of US$5.90/MMBtu (between Henry Hub prices and Asian LNG prices) will be required, while the corresponding price differential required for Canadian terminals (i.e. the difference between Alberta prices and Asian LNG prices) is US$4.75/MMBtu. Note, however, that the production costs for many Canadian producers exceed the domestic hub price (e.g. the break-even domestic price in the Horn River Basin is around US$6.30/MMBtu),[9] so the price differential will need to be higher than the US$4.75/MMBtu estimated for exports from such producers to be profitable.

North American gas producers are at a cost disadvantage compared to producers from established LNG exporters such as Qatar. The long-run marginal costs of production unconventional gas range from US$3-5/MMBtu in the US (and are even higher in Canada), which are among the highest in the world and much higher than marginal costs in Qatar. It should be noted, though, that North American LNG is likely to be competitive against newer escalating-cost supplies of Australian LNG.[10] The costs of many of Australia’s upcoming LNG projects have massively increased due to labor shortages, regulatory burdens and the strength of the Australian dollar. Australia’s estimated break-even prices of $7–11/MMBtu are comparable to the break-even prices of Canadian ($8.35/MMBtu) and US ($9.90/MMBtu) LNG exports.

Impact on Natural Gas Price Differentials

The Asian LNG market is imperfectly competitive ― Asia–Pacific countries such as Japan and South Korea source their LNG imports from a limited number of countries which hold significant market power and can charge high prices. Moreover, the pricing formulas of most long-term Asian LNG contracts tie natural gas prices to the price of crude oil, which has been high in recent years and has thus further contributed to Asian buyers paying the highest worldwide prices for natural gas.

The potential for significant North American LNG export flows to the Asia-Pacific has important implications for Middle East-sourced LNG. Specifically, as North American producers enter the Asian market, the current high price differentials of more than $10/MMBtu (between Asian and North American prices) will become unsustainable, given that price differentials of only around $4.50-$6/MMBTu are required to make trans-Pacific LNG trade economically viable. Asian gas prices are likely to fall relative to North American gas prices, reducing the price differentials.

Interestingly, price differentials could decrease even if actual export volumes are limited. As discussed earlier, because of the cost disadvantage of North American producers, existing producers have the option of reducing the prices they charge Asian buyers, so as to price North American producers out of the market while continuing to maintain their share of the market (albeit with lower profits). In such a scenario, Asian gas prices will have decreased without a significant influx of North American LNG into Asia. There are already indications that Qatari gas producers behave in the manner described above. In response to the growing threat of Australian competition, Qatar reduced its price demands towards Japan last year despite the post-Fukushima surge in Japan’s LNG demand.[11]

In addition, the North American gas supply push may eventually challenge the very basis of Asian LNG pricing: the use of oil-indexed formulas. The North American domestic gas industry has its own benchmarks for pricing (e.g. Henry Hub pricing). The contracts signed by GAIL and KOGAS with Cheniere, for instance, adopt Henry Hub-based pricing. Prices of North American LNG based on gas-hub indices are likely to be lower than prices determined using traditional oil-indexed formulas (at current oil price levels), which could lead buyers to increasingly explore alternative pricing mechanisms for contract LNG. More importantly, it allows Asian LNG buyers to diversify their exposure away from a complete reliance on oil prices alone.

Implications for Middle East LNG Exporters

How do these developments in global LNG markets affect the incumbent Middle East LNG exporters? In 2011, out of a total of 130 billion cubic metres (bcm) of LNG exported out of the Middle East, Qatar accounted for some 79% or 102.6 bcm, while the smaller producers Oman, Abu Dhabi and Yemen accounted for the rest, each producing roughly between 9 to 11 bcm.[12] Qatar alone accounted for 31% of global LNG exports of 330.8 bcm in 2011. In terms of export destination, some 47% of Qatari exports headed to the Asia-Pacific, and 42% went to the Europe and Eurasia region.

Qatar, as the world’s largest single LNG exporter, will be at the forefront of competition with key players in both the European and Asian markets. As an infra-marginal producer with all major capital investments already in place and in the process of being amortized, Qatar occupies a privileged though by no means entrenched competitive position. At the margin, Qatar will be a major competitor for market share in UK and Europe against the oil-indexed pipeline gas exports from Russia. In Asia, both Qatar and Australia will face the prospects of sharing the Asian LNG market with some volumes of US LNG exports indexed to Henry Hub prices by 2020. How market dynamics play out, and to what extent markets get more liberalized with flexible volumes of LNG, priced off trading hubs with gas-on-gas competition increasingly replacing long-term oil-indexed, destination-restricted contracts as the latter expire over the coming years, only time will tell.

[1] BP Statistical Review of World Energy June 2011 (2011).

[2] Golden Rules for a Golden Age of Gas: World Energy Outlook Special Report on Unconventional Gas (Paris: International Energy Agency, 2012).

[3] Are We Entering a Golden Age of Gas? Special Report (Paris: International Energy Agency, 2011), p. 77.

[4] S. Jayasankaran, “Petronas Urges Govt to Stop Gas Subsidies,” Business Times (June 6, 2012); Fitri Wulandari, “Total’s Indonesia Unit Ships First LNG To West Java Terminal,” Bloomberg (April 27, 2012).

[5] “Japanese Protest Over Planned Restart of Nuclear Reactors,” Reuters (June 1, 2012); “Tohoku Outline Summer LNG Needs,” World Gas Intelligence (Mar 30, 2011), pp. 2-3.

[7] “Asian LNG Medium-Term Outlook, World Gas Intelligence” (August 17, 2011), p. 10.

[8] Gas Market Outlook: May 2011 (London: Nexant, May 2011).

[9] “Canada Gas Supplies More Than Ample,” World Gas Intelligence (March 9, 2011), pp. 3–4.

[10] “Asia Oil-linked LNG Term Prices May Nearly Double by 2020–Barclays,” Platts (April 13, 2011).

[11] “Qatar Cuts Price Demands,” World Gas Intelligence (July 6, 2011), pp. 1–2.

[12] BP Statistical Review of World Energy June 2012.

The Middle East Institute (MEI) is an independent, non-partisan, not-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.