Malaysia and the GCC Countries: Fertile Ground for Further Expansion of the Takaful Industry

June 16, 2013

Share

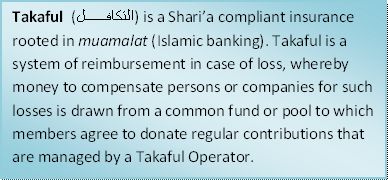

The Takaful industry has expanded rapidly in recent years.[1] In 2011, the industry recorded 19% higher growth than in the previous year. Takaful is generally regarded as a profitable product with ample growth potential. With strong support from industry players, government institutions and increasing awareness among customers, the Takaful industry is expected to develop further in the coming years.

Malaysia and the Gulf Cooperation Council (GCC) countries are key players in the global Takaful market. Their share of the world market currently stands at an estimated 15% and 10%, respectively.[2] Malaysia’s Takaful industry grew at an impressive rate of 24% while the GCC achieved 16% growth in 2011. Saudi Arabia, the largest Takaful market, contributed US$4.3 billion (a 51.8% share of worldwide Takaful). Malaysia ranked second (with a total contribution of US$1.4 billion), followed by the United Arab Emirates (UAE), with a contribution of US$818 million.[3] Given the fact that Malaysia and the GCC countries are among the pioneers in Islamic finance, the achievements of the Islamic insurance industry in these countries is quite significant.

The Takaful industry has become more diverse internationally while the number of Takaful operators operating worldwide has risen dramatically. The GCC countries are at the leading edge of the global Takaful industry. According to the latest industry data, the GCC region contributed more than 62% of global premiums and accounted for 40% of total Takaful business. Of the 200 Takaful operators worldwide as of 2012, 77 are based in the GCC region. Malaysia is a key player in the worldwide Takaful sector in its own right. It is home to 16 Takaful operators. Malaysia’s contributions per operator are equal to those of Saudi Arabia and twice those of their other GCC counterparts. Ernst & Young’s World Takaful Report 2012 notes that global Takaful contributions reached US$8.3 billion in 2011. Deloitte’s recent study, The Global Takaful Insurance Market: Charting the Road to Mass Markets, reports that the Takaful business could well reach US$20 billion by 2017.[4]

Factors Spurring the Growth of Takaful

Several factors have driven the expansion of the Takaful industry in Malaysia and GCC countries. For one thing, strong economic growth in these countries and the rise of middle-income earners, has led to increased purchasing power among Muslim customers (which are the main target of this product). For another, there is increasing public awareness of the existence and benefits of insurance and financial protection, especially syariah-compliance products. In addition, in the case of Malaysia, government support for creating an efficient, progressive, and comprehensive Islamic financial system has contributed significantly to the effectiveness and efficiency of the Malaysian Islamic financial sector.

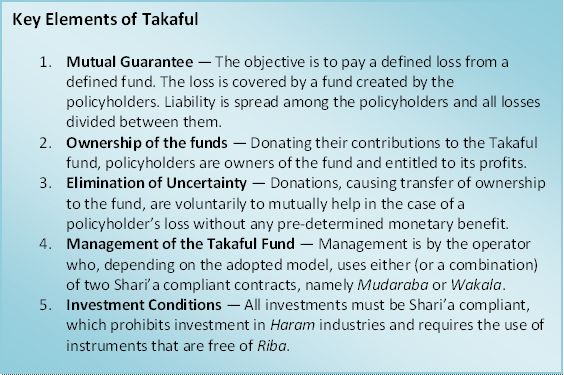

Market segmentation shows that Islamic insurance has been predominantly concentrated on family Takaful (i.e., life insurance) and medical Takaful, despite the fact that the industry also offers property and motor/general Takaful.[5] According to the Ernst & Young report, medical Takaful contributed significantly to Takaful industry growth in the GCC countries while family Takaful has emerged as the dominant business line in Malaysia (amounting to nearly two-thirds of the Takaful gross contribution).[6] Contributions to motor/general Takaful products are relatively low compared to family and medical Takaful. This is believed due to the fatwa permitting Muslim consumers to opt for conventional motor/general insurance products.[7]

Future Direction

Despite the strong contributions to the Takaful industry, the key markets in the Arab Gulf, Bahrain, Qatar, UAE, Kuwait and Saudi Arabia, have witnessed a slower pace of growth. Takaful contributions in those countries which provide about half of all such contributions grew, on average, at a mere 10% in 2010, compared with a compound annual growth rate (CAGR) of 41% during the period 2005–2009. Bahrain and UAE suffered the steepest decline in growth rates, from 55% to 17% and from 98% to 28%, respectively.[8]

However, this dark cloud has a silver lining. The populations of the GCC countries are expected to increase significantly in the years ahead. Moreover, their demographics are changing. According to Sohail Jaffer, “the region has a very young population with approximately 70 per cent in the 15–64 years bracket and according to World Bank forecasts; the total population of the GCC will grow by an average of 2.4 per cent per year in the next 5 years taking it to 45.6 million in 2015. As this young population in the region matures the demand for financial products would see a tremendous increase.”[9] Thus, it is reasonable to expect that the demand for Family Takaful will increase in the near future.

There is also great potential for the Takaful industry in the Arab Gulf to expand to countries in other regions, such as Kenya and South Africa. GCC Takaful companies also have potentially huge opportunities to expand their business in Europe (including in the UK, France, Germany, and Turkey) and in Asia markets such as India and Indonesia.[10] The rest of the Middle East and North Africa (MENA) region, too, offers tremendous growth potential for GCC companies to tap.

Across the Arab Gulf, the utilization of banking institutions known as bancatakaful has been the preferred approach and has proven to be the most efficient channel in distributing Islamic insurance products. Unlike countries in Southeast Asia that greatly benefited from the use of agency, bancatakaful has proven very successful in the distribution of family Takaful products in the GCC countries. Through the banks’ financial planning and wealth management, the Takaful product is marketed directly to bank customers, and tailor-made family Takaful products might also be offered.[11] The close relationship and good reputation between banks and customers has contributed to the marketability of Takaful products in the region.

According to Tobias Frenz, CEO at Munich Re, Malaysia has been a pioneer in Islamic banking and finance industry and is widely acknowledged as having the biggest and most developed Takaful worldwide.[12] Over the years, Malaysia has equipped its Islamic financial sectors with the necessary regulatory and infrastructures to achieve this status. The Takaful Act (1984) was introduced to protect the industry. The Act also served as a milestone in promoting the industry at the local as well as global levels. A cadre of committed regulators actively supporting the entire value chain of Islamic finance have also helped the industry to grow. In addition, a number of measures have been introduced to bring Islamic insurance into the mainstream of Malaysia’s insurance industry, including:

Given the intensive planning and activities of the Islamic finance sector in Malaysia, particularly the Takaful industry, some suggest that the Takaful industry in Southeast Asia could become three times as large as that of the Middle East by 2015.[13] This is also supported by the large Muslim markets among Malaysian neighbors, Indonesia and Brunei, as well as the strong growth of business in Singapore that actively attracts Arab investors.

Conclusion

Although the Takaful industry has seen double-digit growth since 2010 and has been successfully developed, the industry has also been struggling to deal with several decisive issues in both Malaysia and the GCC countries. These include lack of penetration particularly in vibrant markets, lack of awareness and acceptance among large segments of Muslim populations, regulation and governance issues, a shortage of talent and qualified practitioners, lack of innovative products, and a limited investments avenue for Takaful funds. Therefore, boosting the further expansion of Takaful in both Malaysia and the GCC countries requires that strong measures be taken to increase public awareness, improve operational efficiency, and ensure high-quality training.

Encouragingly, the market for the Takaful industry has spread all over the world. Although it is widely recognized that Malaysia and GCC have made significant contributions, less well known but important is the entry into the Islamic finance industry of countries such as Sudan and Indonesia. In fact, Sudan is now regarded as the largest Takaful market outside Malaysia and GCC. This development could be seen as a good competition in industry and at the same time brings huge opportunities to Takaful companies in Malaysia and GCC to synergise their business with their counterparts in the new emerging companies in those particular nations. There is considerable potential for Malaysian and GCC Takaful operators to tap into regional and international markets, thereby enhancing their own positions and exporting their knowledge and experience.

[1] Regarding the development of the takaful industry in Malaysia, see Jacky Lim, Muhammad Fahmi Idris, and Yuri Carissa, “History, Progress, and Future Challenge of Islamic Insurance (Takaful) in Malaysia.” Paper delivered at the 2010 Oxford Business and Economics Conference, St. Hugh’s College, Oxford University (June 24–26, 2010), http://www.academia.edu/953632/History_Progress_and_Future_Challenge_of….

[2] Ernst & Young, The World Takaful Report 2012: Industry Growth and Preparing for Regulatory Change (April 2012), www.ey.com/mena.

The Middle East Institute (MEI) is an independent, non-partisan, not-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.

The Takaful industry has expanded rapidly in recent years.[1] In 2011, the industry recorded 19% higher growth than in the previous year. Takaful is generally regarded as a profitable product with ample growth potential. With strong support from industry players, government institutions and increasing awareness among customers, the Takaful industry is expected to develop further in the coming years.

The Takaful industry has expanded rapidly in recent years.[1] In 2011, the industry recorded 19% higher growth than in the previous year. Takaful is generally regarded as a profitable product with ample growth potential. With strong support from industry players, government institutions and increasing awareness among customers, the Takaful industry is expected to develop further in the coming years. Malaysia and the Gulf Cooperation Council (GCC) countries are key players in the global Takaful market. Their share of the world market currently stands at an estimated 15% and 10%, respectively.[2] Malaysia’s Takaful industry grew at an impressive rate of 24% while the GCC achieved 16% growth in 2011. Saudi Arabia, the largest Takaful market, contributed US$4.3 billion (a 51.8% share of worldwide Takaful). Malaysia ranked second (with a total contribution of US$1.4 billion), followed by the United Arab Emirates (UAE), with a contribution of US$818 million.[3] Given the fact that Malaysia and the GCC countries are among the pioneers in Islamic finance, the achievements of the Islamic insurance industry in these countries is quite significant.

Malaysia and the Gulf Cooperation Council (GCC) countries are key players in the global Takaful market. Their share of the world market currently stands at an estimated 15% and 10%, respectively.[2] Malaysia’s Takaful industry grew at an impressive rate of 24% while the GCC achieved 16% growth in 2011. Saudi Arabia, the largest Takaful market, contributed US$4.3 billion (a 51.8% share of worldwide Takaful). Malaysia ranked second (with a total contribution of US$1.4 billion), followed by the United Arab Emirates (UAE), with a contribution of US$818 million.[3] Given the fact that Malaysia and the GCC countries are among the pioneers in Islamic finance, the achievements of the Islamic insurance industry in these countries is quite significant. The Takaful industry has become more diverse internationally while the number of Takaful operators operating worldwide has risen dramatically. The GCC countries are at the leading edge of the global Takaful industry. According to the latest industry data, the GCC region contributed more than 62% of global premiums and accounted for 40% of total Takaful business. Of the 200 Takaful operators worldwide as of 2012, 77 are based in the GCC region. Malaysia is a key player in the worldwide Takaful sector in its own right. It is home to 16 Takaful operators. Malaysia’s contributions per operator are equal to those of Saudi Arabia and twice those of their other GCC counterparts. Ernst & Young’s World Takaful Report 2012 notes that global Takaful contributions reached US$8.3 billion in 2011. Deloitte’s recent study, The Global Takaful Insurance Market: Charting the Road to Mass Markets, reports that the Takaful business could well reach US$20 billion by 2017.[4]

The Takaful industry has become more diverse internationally while the number of Takaful operators operating worldwide has risen dramatically. The GCC countries are at the leading edge of the global Takaful industry. According to the latest industry data, the GCC region contributed more than 62% of global premiums and accounted for 40% of total Takaful business. Of the 200 Takaful operators worldwide as of 2012, 77 are based in the GCC region. Malaysia is a key player in the worldwide Takaful sector in its own right. It is home to 16 Takaful operators. Malaysia’s contributions per operator are equal to those of Saudi Arabia and twice those of their other GCC counterparts. Ernst & Young’s World Takaful Report 2012 notes that global Takaful contributions reached US$8.3 billion in 2011. Deloitte’s recent study, The Global Takaful Insurance Market: Charting the Road to Mass Markets, reports that the Takaful business could well reach US$20 billion by 2017.[4]