This paper is based on the first of a series of workshops on “Perceptions of Decision Makers in Gulf Cooperation Council States towards Strategic Security Ties with China,” organized by the Department of International Affairs and the Center for Humanities and Social Sciences at the College of Arts & Sciences, Qatar University, 12/15/15. More …

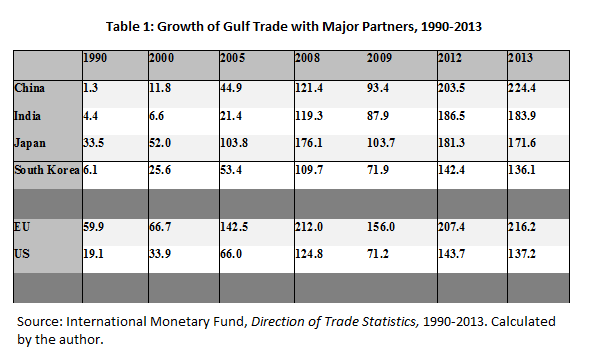

As has been widely acknowledged, the balance of the GCC’s external trade has changed fundamentally over the past decade. China and India have been the major beneficiaries of the shift. The significance of the change can be best understood within the context of the Gulf region’s long-term economic and political connections. For the two centuries preceding 2013, the bulk of Gulf trade was with Western countries.[1] Trade with Japan became important from the 1970s onwards, so much so, that Japan became the second largest trading partner for the Gulf region from the late 1970s until 2011.[2]

In 2013, for the first time, China became the largest trading partner of the Gulf region (taking all eight Gulf countries together). Trade with the European Union (EU) was pushed into second position, with India taking the third position. Table 1 provides data on how the Gulf’s trading pattern have changed from 1990—when China and India were relatively marginal in Gulf trade—through to 2013 which was the first year in which China became the leading trading partner of the 8 Gulf states. Figures for 2014 show China pulling even further ahead, with China’s total standing at $255 billion, and the European Union’s at $232 billion.[3]

The European Union remains at present the largest trading partner of the GCC, but current rates of trade growth—and the growing demand for imported Gulf oil in China and India—mean that the China’s trade is likely to overtake that of the European Union by 2020. A study of likely GCC trading developments undertaken by the Economist Intelligence Unit in 2014 states:

By 2020, the largest share of GCC exports will go to China, at around US$160bn … China will also dominate the import market, providing about US$135bn of goods to the Gulf, nearly double the value in 2013. China’s increasing share of GCC exports matches its economic rise, with growth tripling since 2001 to reach 12% in 2013, and now providing 14% of GCC imports. GCC trade with China grew more rapidly during 2010-13 than with any other significant trade partner, at a rate of 30% for exports and 17% for imports. [4]

Even at present, China is by far the largest trading partner for Oman, and stands not far short of the European Union in trade with Saudi Arabia.

It has been argued by some that trade figures alone may not give a true picture of the real strength of an economic relationship and its significance, and that China’s economic relationship with the Gulf may not be as significant as the trade figures suggest. Wider dimensions—such as the character of the trade, and also the extent of investment flows and contracting—are certainly worth noting. From a Chinese perspective, Gulf trade constitutes a mere 3 percent of China’s total trade. While the trade may be significant to the Gulf economies, it is dwarfed on the Chinese side by trade with other countries and regions. However, some 35 percent of China’s Gulf trade is composed of imports of Gulf oil, which is critical to the further growth of the Chinese economy.

It has been estimated that China will account for about 43 percent of the increase in world oil consumption over the next decade.[5] The trade with the Gulf, moreover, makes up about 70 percent of its trade with the Arab world. China’s economic stake in this strategically significant region, therefore, is focused very much on the Gulf. It is also significant that Chinese trade is spread across all Gulf countries, rather being concentrated in any one state. In this respect it differs significantly from US-Gulf trade, approximately half of which is accounted for by Saudi Arabia alone.

Chinese companies have, moreover, been winning contracts for major construction projects in the region in recent years, such as that for construction of the culturally sensitive Haramain High Speed Rail Project, and for the Waad Al-Shamal phosphate plant in Saudi Arabia. In 2013 Chinese ambassador to Saudi Arabia Li Chengwen stated that there were 140 Chinese companies, the bulk of which were in the construction, telecommunications, infrastructure and petrochemicals sectors. The value of their projects, he stated, came to about $18 billion.[6] Investment flows in both directions (GCC to China and vice versa), have also begun to have an impact. Most of these have been in the field of petrochemicals. Up to the present, however, the record here has been mixed, with the negotiation process being protracted and not always leading to a positive result.

Overall, then, the extent and the significance of the reorientation in the GCC’s pattern of economic relations in recent years is clear. What is of interest now is how the new relationships with East and South Asian countries will be handled, and how the GCC will relate to the regional networks which China is developing as part of its wider global strategies. The next section will outline what the developing networks are, while the final section considers whether and how the GCC could relate to them.

The Wider Networks of China’s Strategies

China’s global strategies operate at different levels. At one level there is a concern with maintaining workable relations with the United States, recognizing that China’s interests (economic and political) will be damaged by a confrontation with the sole existing superpower. China, it is said, must avoid the mistakes made by Germany and Japan in the 1930s, and must seek a global role not by confronting the existing power structures but by integrating China into the system of global power and influence. The latter comprises not just the United States and its allies, but also the web of international institutions (i.e., the IMF., UN bodies, the World Bank, etc.) through which they influence and perhaps control global developments.

At another level, Chinese policies seek to build up alternative networks of coordination and cooperation, within which China can play a prominent if not predominant role. Of key importance here are the BRICS (Brazil, Russia, India, China and South Africa) grouping and the Shanghai Cooperation Organization (bringing China and Russia together with the Central Asian former Soviet Union states, and now joined by India and Pakistan). In addition to the institutions within those bodies that have been created to enhance cooperation and development, the Chinese government has created its own institutions and programs to establish a solid basis on which to build cooperative relations in the heartland of its nascent network—East, Central, and Southeast Asia. A key institution is the Asian Infrastructure Investment Bank (AIIB), and the main programs are those of the One Belt One Road (OBOR) and the Maritime Silk Road (MSR). The latter initiatives seek to create, through massive investment in infrastructure, the land and sea communications channels through which China can interact with, and integrate itself into, the Eurasian region as a whole.

The programs cover not only construction of the necessary transportation infrastructure but also the creation of the industrial and financial infrastructure necessary for effective development in the Central Asian states, in particular. Such development is needed not only for the Central Asian economies to constitute effective regional partners for China, but also to ensure long-term political stability in the region. Unstable regimes, with populations prone to political or religious extremism, would threaten China’s westward communications and perhaps also create ethnic tensions within China—with a negative impact on the coherence of China’s own polity.

The scope and importance of what is being developed with the OBOR and MSR is impressive, and will clearly affect future patterns of economic interaction and development throughout Asia, with implications for African countries as well. Although the OBOR and MSR programs were only made public in September 2013, substantial progress has already been made in planning—and in some cases beginning work on—the necessary infrastructure. The location of the main arteries for OBOR and MSR have not always been clear, or were left deliberately imprecise until regional reactions could be assessed. The map provided in Figure 1, however, was issued by China’s state news agency Xinhua in March 2015 and can therefore be seen as representing the official view. In practice, the extent of the infrastructural connectivity which the Chinese government is creating is more widespread than the map suggests. The OBOR land routes link up with other road and rail schemes (planned or under implementation) that link China to its neighboring regions. These crucial regions the route will link to include China-Pakistan Economic Corridor (leading from China’s Xinjiang region to the Pakistani port of Gwadar),[7] the Kunming-Singapore Railway (running from China’s Yunnan province through South-East Asia to Singapore),[8] and the Bangladesh, China, India, and Myanmar Economic Corridor (which begins in Kunming and ends in Kolkata).[9] There is also likely to be a ‘northern route’ high-speed link between Beijing and Moscow.

Linking the GCC to the  Developing Networks

Developing Networks

In the official Xinhua map of the OBOR and MSR, it is clear that the main communications routes do not lead to or through the Gulf. The One Belt One Road, as currently envisaged, passes through the northern part of Iran (with Tehran on the route), without any provision for an extension to the GCC states—although statements made by President Xi Jinping during his visit to Saudi Arabia made reference to the desirability of the GCC countries being linked in to the OBOR project.[10] The reason why a GCC-OBOR link is not currently envisaged clearly lies in the conflictual state of relations across the Gulf. The creation of major transnational land communications (combining in this case not only road and rail links but also oil and gas pipelines) requires close coordination and cooperation between the governments concerned. Given the confrontational relations between Saudi Arabia and Iran, in particular, there is no basis for collaborative planning, collective management or even practical dialogue. The GCC stands to lose more from this than Iran.

The Xinhua map also reveals that the major sea lanes of the Maritime Silk Route similarly bypass the Gulf, albeit passing through the Red Sea. The main eastward route from China crosses the Indian Ocean and heads straight to the Kenyan ports of Lamu and Mombasa. This, indeed, reflects ongoing realities. China is investing heavily in the Kenyan ports, building up facilities which will serve the markets of the East African region as a whole. Further infrastructural investment (mainly financed by the Kenyan government, but with some Chinese involvement) is projected, intended to secure easy access to regional markets. The most significant of these is the LAPSSET, a project which involves rail, road, and pipeline systems connecting the new port facilities in Lamu to northern Kenya, Ethiopia, and South Sudan, complementing the lines of communication running from Mombasa through Nairobi to Uganda. Whereas some Chinese companies have in the past used the GCC (Dubai in particular) as a stepping stone for their activities in the Western Indian Ocean, in the future there will be little need for a stepping stone. China will also be able to use the port of Gwadar in Pakistan for transhipment goods in the Western Indian Ocean region, without the need for its ships to enter the Gulf.

In itself, the possible marginalization of the GCC in the OBOR and MSR initiatives may not matter. China and the GCC will remain important to each other economically whatever happens to the wider networks of communications. Their existing trade is based largely on maritime links, and these can continue as before. Both sides have a strong interest in continuing their relationship, and if possible developing it further.

There is, however, a political loss which the GCC would incur by staying aloof from the developing communications networks. As indicated earlier, the new communications networks stem from, and are integrated into, an alternative structure of power in global politics. The institutions which finance them and support them are outside the circle of institutions that have dominated the global political economy since WWII. If the GCC finds ways of relating to the new networks, its economic strength will ensure that it can play a significant role in the new global power structures. This does not necessarily imply transferring its allegiance away from its existing close relations with Western countries and institutions, but rather complementing these with an emerging and potentially very significant strand of contacts and engagement. Iran, benefiting from its geographical advantage (adjacent to Central Asia), has already positioned itself so as to benefit from these new international relationships; it is poised to become a member of the Shanghai Cooperation Organization, and has welcomed inclusion in the One Belt One Road project. Trade between Iran and China, it was announced at the end of the recent visit of President Xi Jinping to Iran, is projected to increase dramatically by 2020.[11]

While the confrontation between Saudi Arabia and Iran makes the proposal for an OBOR-GCC link difficult, the OBOR project could also ultimately provide an incentive for dialogue. Both Iran and the GCC would benefit if the GCC could be linked to OBOR through Iran. China, having good relations with both Saudi Arabia and Iran and with interests of its own at stake, would be in a good position to initiate and shape a dialogue.

[1] There was, of course, substantial trade with India when India was under the British Raj. This, however, can be counted as part of the “Westward trade”, in so far as the trade was linked into Britain’s global trading networks.

[2] Japan’s ranking declined after 2011, such that by 2013 it had fallen to fourth position.

[3] “GCC Trade and Investment Flows,” Economist Intelligence Unit, (2014), 9-10, http://www.economistinsights.com/countries-trade-investment/analysis/gcc-trade-and-investment-flows-0.

[4] Ibid, p 9.

[5] “BP Energy Outlook 2035, Country and Regional Insights – China” (London: BP, 2015).

[6] “Saudi-Chinese Trade Increases by 14 Percent,” Asharq al-Awsat, November 20, 2013, http://english.aawsat.com/2013/11/article55323012/saudi-chinese-trade-i….

[7] Lal Khan, “China-Pakistan Economic Corridor,” Daily Times, December 6, 2015, http://www.dailytimes.com.pk/opinion/06-Dec-2015/the-china-pakistan-eco….

[8] “Singapore to Kunming by High Speed Train,” Malay Mail Online, October 29, 2014, http://www.themalaymailonline.com/travel/article/singapore-to-kunming-b….

[9] Atul Aneja, “China, India Fast-Track BCIM Economic Corridor,” The Hindu, June 26, 2015, http://www.thehindu.com/news/national/china-india-fasttrack-bcim-econom….

[10] Wang, Fengfeng, Li Jianmin, “Xi Wraps Up Historic Visit to Saudi Arabia, Steps Up Energy Cooperation,” Xinhua, January 21, 2016, http://news.xinhuanet.com/english/2016-01/21/c_135029295.htm.

[11] “Iran and China Agree Closer Ties After Sanctions Ease,” BBC News, January 23, 2016, http://www.bbc.co.uk/news/world-middle-east-35390779.

The Middle East Institute (MEI) is an independent, non-partisan, not-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.